4 Unbelievable Solutions To The Debt Ceiling Crisis

These are going to sound super crazy, but they just might work.

Sometime between June and September, the U.S. government could default on its debt, sending the world’s largest economy over a cliff.

But this nightmare scenario isn’t a foregone conclusion.

Even if Congress can’t get its act together and raise the debt ceiling, there are still four ways to avoid a calamity.

These are going to sound super crazy, but they just might work. I’m going to go from least crazy to most crazy.

Solution #1

The first potential solution is to have the Treasury department prioritize payments to bond holders over everyone else.

This means putting bond holders ahead of retirees and their social security payments, ahead of funding for the military, and ahead of all of the government’s other programs and services.

In this scenario, the government would only spend the amount of money it receives through taxes. Any spending beyond that would be cut.

This obviously would lead to a deep recession and the markets might still look at it like a default because even though the government is paying bond holders, it’s not paying all of the other parties which it owes money.

Additionally, Treasury Secretary Janet Yellen has said that this type of prioritization just isn’t possible based on the way the Treasury Department’s systems are set up.

So this isn’t a great solution.

Solution #2

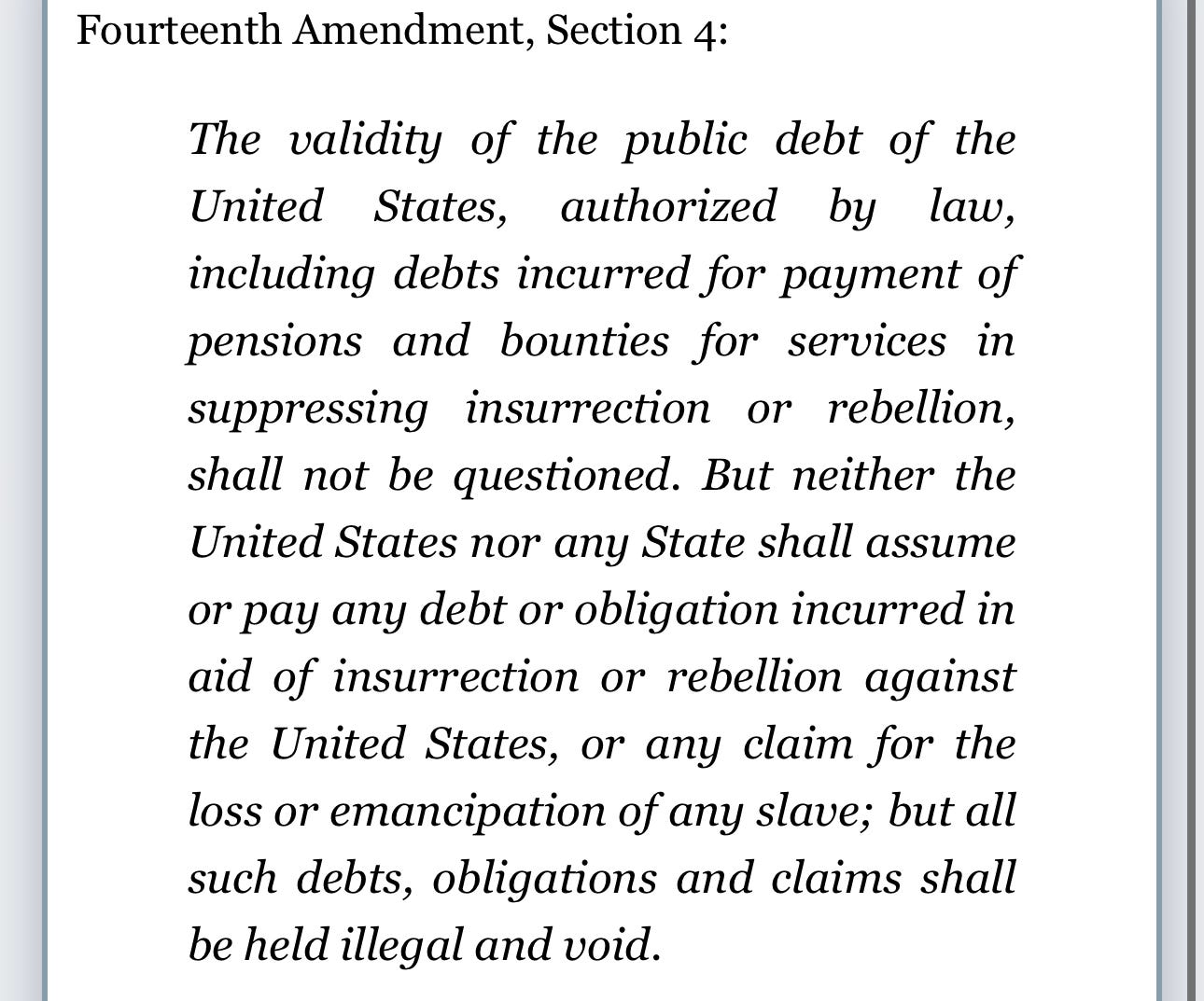

That brings us to solution number two, which might be the least messy of the four options I’m going to discuss. This entails having the President invoke the 14th amendment of the constitution.

Within the 14th amendment, there is a section that says that “the validity of the public debt of the United States…shall not be questioned.”

The 14th amendment was passed in 1866, a year after the Civil War ended. Some scholars say that this text was added to the Constitution to ensure that representatives from former Confederate states wouldn’t try to weaken the United States by threatening to not pay the country’s debt.

Under a similar interpretation, this could mean that it’s unconstitutional for the U.S. government to default on its debt today, and so the president and his Treasury department can just ignore the debt ceiling and keep borrowing money.

Solution #3

Next up is solution three, which is for the Treasury Department to issue extremely high coupon bonds. This one is a little esoteric if you’re not familiar with bond math, but think of it like this:

The U.S. government borrows money by issuing bonds with a certain face value. Once those bonds reach maturity—whether it be 1 year, 10 years or 30 years from the date of issuance—the holder of the bonds gets the face value back.

But between the period when the bond is issued and paid back, the government also pays the bond holder coupons. Usually, the coupon rate is similar to the market interest rate—something like 3%, 4% or 5% like it is today.

A $100 face value bond would pay $5 in coupons per year ($100 x 5%) if the coupon rate is equal to the market interest rate of 5%.

But the coupon rate on the bond and the market interest rate don’t have to be the same. There’s nothing to stop the government from offering a much higher coupon rate—10%, 50%, 100% or more.

If it offered a 100% coupon rate, then the $100 face value bond would pay $100 in coupons per year ($100 x 100%). How much would you be willing to pay for that bond if market-based interest rates are 5%?

You’d be willing to pay much, much more than $100. If you do that math, then a 10-year bond with a face value of $100 paying a 100% coupon would be worth $840 today.

So in this situation, the government could sell a $100 face value bond for $840. And if it offered an even higher coupon rate, it could sell it for even more.

Now here’s the important part: only the face value of the bond counts towards the total debt issued by the government.

So by using high coupon bonds, the government could raise a lot of money while increasing the amount of debt that counts towards the debt ceiling by a much smaller amount.

That’s the magic of bond math.

Solution #4:

Finally, we have the fourth solution, which might be the craziest one yet. It involves having the Treasury mint a $1 trillion platinum coin.

I know this sounds absurd, but based on a 20-year-old law, the Treasury department can order the U.S. mint to create platinum coins of any denomination. So, theoretically, it could mint a $1 trillion coin, deposit it at its account at the Federal Reserve and then spend it—all without raising the debt ceiling.

Now you might be thinking, “Printing money out of thin air—won’t that cause inflation?”

Well, it could, but probably not as much as you might think.

Because remember, even with the $1 trillion coin, the government would still only be spending money that it’s already been authorized to spend by Congress. This is spending that would have happened anyway.

So, there’s no new spending.

But, as the government spent its $1 trillion, behind the scenes there would be some changes to the composition of money within the banking system.

Reserves, or money held by banks at the Federal Reserve, would increase, which could put downward pressure on interest rates. That isn’t something we want in the current environment where the Fed is trying to bring inflation down.

That could be offset by the Fed if it sells some of the bonds on its balance sheet, but it gets pretty messy and you have a situation where the Treasury department starts to influence monetary policy, which hurts the independence of the central bank.

As you can see, the $1 trillion coin isn’t ideal, but it’s an option.

Legal Challenges

So there you have it—four really crazy and untested solutions that could be used to avoid a catastrophic U.S. government default.

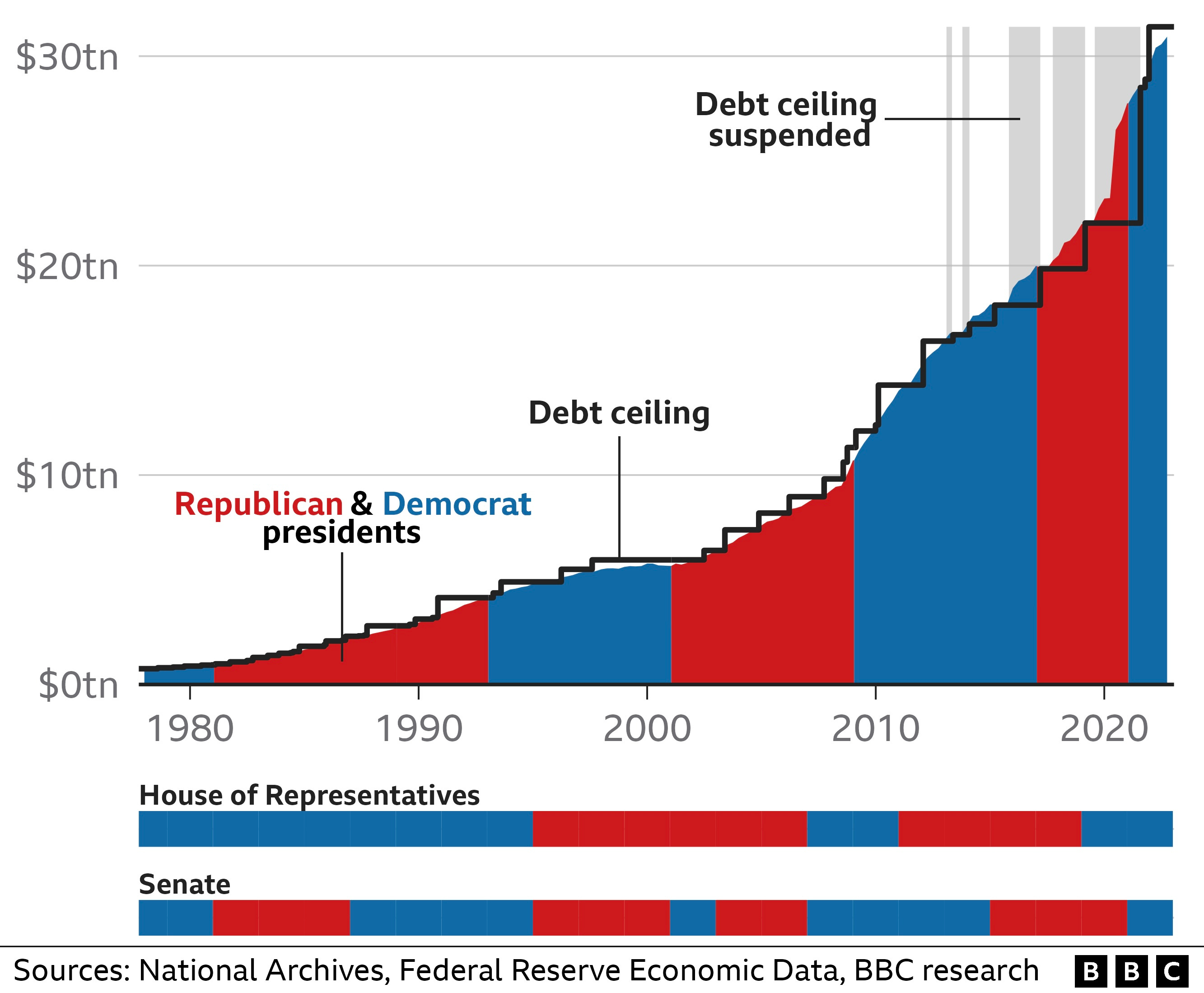

Of course, it’s better that these solutions stay untested and we get through this mess by having Congress raise the debt ceiling as its done 78 times over the last six decades.

That’s especially the case because, even if these alternative solutions end up working, they will most likely be subject to legal challenges.

And in the time between when the solutions are enacted and when we have a clear judgement about whether they’re legal, there will be a ton of uncertainty, which will create havoc in financial markets and the economy.

It’s much better if we don’t have to deal with that.