A Simple Guide To Bonds

There's plenty of opportunity in the worst year ever for bonds.

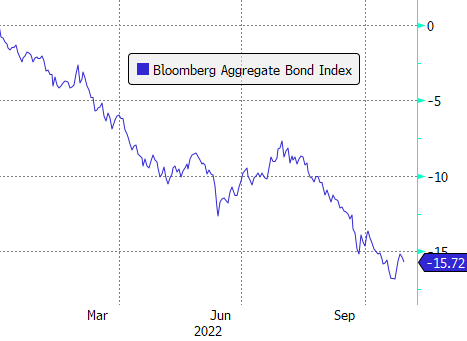

Bonds are having their worst year in history. That’s not an exaggeration— their worst year on record going all the way back to 1794.

The most popular benchmark for bond market performance, the Bloomberg US Aggregate Bond Index, is down 15.7% so far this year—nearly double 1969’s 8.1% decline, which up until 2022, was the worst year for bond markets in the past century.

By bond market standards, what we are seeing in 2022 is a catastrophe. But in every down market, there is opportunity and the bond market is no different. Bonds today are offering their highest interest rates in 15 years, and the great thing is, there is something for everyone.

Whether you are risk averse or you have a high risk tolerance, there is an opportunity to make money with bonds.

Why Bonds Are Tumbling

The reason bonds have been doing so poorly this year is simple: sky high inflation.

For nearly 40 years, interest rates have been steadily declining, but this year, they’ve rocketed higher because of inflation. Starting in March, the Federal Reserve embarked on a rate hiking campaign that’s picked up steam as it’s gone on, turning into the most aggressive monetary policy tightening since 1980.

Rising interest rates are bad news for bond investors since a bond’s price moves in the opposite direction to that of rates. Thus, while interest rates have been going up, bond prices have been going down.

This year’s sell-off aside, if you look throughout history, bonds have been a fantastic investment. They provide consistent income that is uncorrelated with other financial assets like stocks.

Bonds are generally safer than stocks, but despite that safety, there have been long periods of time when they have actually delivered higher returns. For example, between 1981 and 2011, long term Treasury bonds gave you annual returns of 10.7% versus 10.4% for U.S. stocks, according to data from Edward McQuarrie, a retired professor at Santa Clara University.

The returns for bonds come from price fluctuations and interest payments. This year, bond returns have been abysmal because their prices have fallen, but longer-term, most of the returns from bonds will come from interest payments.

That’s what makes what happened this year an opportunity. Interest rates have spiked to their highest levels in more than a decade, so your potential future returns as a buyer of bonds today is much higher than it would have been if you bought last year.

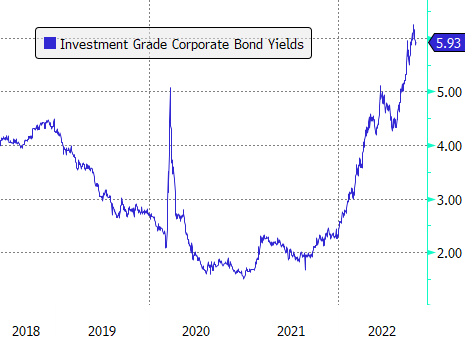

Just to give you an example, the 10-year Treasury—one of the safest investments in the world—is currently yielding 4.04%, more than double the rate of one year ago. Similarly, high quality corporate bonds are giving you almost 6% per year versus 2.25% last year.

Higher interest rates are a good thing for anyone buying bonds today.

There is also another benefit of interest rates being higher, and that is, bond prices are low (bond prices and yields move inversely).

That means that there is now much more potential for price appreciation in bonds if interest rates go back down again. Usually, bonds—especially Treasury bonds— are a great hedge against economic downturns because interest rates tend to fall and bond prices tend to go up when the economy slows or shrinks.

This time around, even though recession risks are rising, bond prices haven’t been going up because we are dealing with a very unique situation with inflation. But in most economic downturns, deflation is more of a concern than inflation, and so bond prices go up and interest rates go down.

If that happens, as a bond investor, you benefit from that price appreciation, which gives you added returns on top of the interest payments you get. It’s also why bonds have historically been a great hedge against recessions, black swans and all types of negative shocks.

What Could Go Wrong

As attractive as bonds look today, nothing is a sure thing. What could go wrong?

With bonds, it’s simple.

If inflation continues to run wild for months and months, then interest rates might move even higher than they are today, and bond prices could decline further. If the 10-year Treasury bond yield shoots up 5% or 6%, then the price of the bond could drop another 7.5% to 15% percent.

With bonds, though, there are safeguards against losses. If you hold the bond until maturity in 10 years, you’d get all your money back, or if interest rates fell back to where they are today, you’d also get your money back.

But temporarily you could see big losses; and if you buy riskier bonds than Treasuries, there’s a chance you might not get paid back at all.

Bond Risks

The easiest way to think about bonds is to consider them loans— loans that can be traded among investors. A bond issuer—usually a government or a company—sells bonds to raise money.

An investor then owns that bond and gets paid interest while they hold it. Then, assuming the bond issuer has the money available, the investor gets paid all their money back on some future date.

Every bond can be judged based on two criteria: credit risk, or how likely it is that you’ll get paid the money you’re owed; and interest rate risk, or a bond price’s sensitivity to changes in interest rates.

Interest rate risk is tied closely to a bond’s maturity, or how far in the future an investor will get paid their money back.

The longer the period between when you buy a bond and when you get paid back in full, the more sensitive that bond’s price is to changes in interest rates (remember that bond prices go up when interest rates go down; and they go down when interest rates go up).

So, you can judge almost all bonds based on these two criteria—credit risk and interest rate risk.

You have bonds with zero credit risk, like U.S. Treasuries, and you have very risky bonds, like junk bonds that are issued by small companies— where you’re not completely sure if the bond issuer will pay you back.

Similarly, you have bonds with very little interest rate risk, like 3-month Treasury bills, that are paid back shortly after you buy them—and bonds with very high interest rate risk, like 30-year Treasury bonds—that aren’t paid back for decades.

Bond Issuers

The biggest issuers of bonds in the U.S. are governments and corporations, and so the most common types of bonds are Treasury bonds, municipal bonds and corporate bonds.

Treasuries are considered the safest type of bonds because the federal government can always create more money to pay you back.

Munis are slightly riskier, but they also considered extremely safe. There’s an added bonus with munis in that you often don’t have to pay federal taxes on the interest you get from those bonds, and if you buy a muni issued by your own state, you often don’t even have to pay state taxes either.

As you might guess, corporate bonds are generally riskier than bonds issued by governments, but the level of risk varies widely. You have cash- rich, low-risk borrowers like Apple to very risky “junk-rated” issuers where there is a real risk of not getting paid back.

Ways To Invest In Bonds

You can invest in bonds by buying individual bonds or bond funds.

The benefit of an individual bond is you can hold it until maturity, and unless the issuer of that bond defaults, you are guaranteed to get your money back at maturity. Another benefit is you can lock in an interest rate until the individual bond matures.

Bond funds hold baskets of many different bonds. They are diversified and super easy to trade. But most bond funds don’t hold bonds all the way to maturity. They kick them out and add new bonds into their portfolio based on their investment objective.

For instance, the iShares 7-10 Year Treasury Bond ETF (IEF) won’t hold bonds with less than seven years until maturity. If a bond gets to that point, it’ll be kicked out and replaced with a new bond. Since bond ETFs never mature, you can hold them indefinitely.

With individual bonds, as long as the bond issuer doesn’t default—you’ll get all your money back if you hold to maturity or interest rates are at the same level or lower than when you bought the bond.

On the other hand, bond funds don’t hold bonds until maturity. So, assuming there are no defaults in the portfolio, you only get your money back if interest rates are the same or lower than when you bought the fund. This only refers to your principle; you’ll keep getting interest payments either way.

Deciding What Bonds To Buy

The first thing to do when deciding what bonds to buy is to figure out how long you want to keep your money invested.

For the sake of simplicity, we can say there are two holding periods: one year or less and more than one year. If you aren’t sure how long you want to hold, then to be safe, consider yourself in the one year or less group.

After figuring out your holding period, you should decide what your investment objective is. Is it to simply preserve the purchasing power of your money against inflation? Is it to earn more interest than you can get with your bank account? Or is it to profit if interest rates go down?

Once you’ve identified your holding period and your primarily investment objective, you can move on to figuring out how much risk you want to take.

As I wrote earlier, bond risk comes in two forms: credit risk and interest rate risk. You can completely do away with credit risk by buying Treasuries issued by the U.S. government and you can almost completely get rid of interest rate risk by buying very short-term bonds that mature in less than a year.

Another way to eliminate interest rate risk is by matching your holding period to a bond’s maturity. For instance, if you have a five-year holding period, you can buy a 5-year Treasury bond, hold it until the bond matures, and get all your money back plus interest.

The price of the bond might go up and down over the course of those five years, but as long as you hold that bond until maturity, you’ll get all your money back.

That said, in some cases you might be willing to take more risk to get higher returns.

Today, Treasuries are offering interest rates of anywhere from 4% to 4.5% with no credit risk, which is great. But what if you want even higher interest rates, in the 5% to 7% range?

Well, then you can consider municipal bonds and investment grade corporate bonds. These bonds aren’t super high risk, but unlike Treasuries, they do have some credit risk—so diversification is critical when buying them. That’s why I suggest looking at ETFs like iShares National Muni Bond ETF (MUB) and the Vanguard Intermediate-Term Corp Bond Index Fund ETF (VCIT) if you are going to invest in these types of bonds.

They hold many, many bonds, so you won’t be hurt much if one or even a handful of bond issuers defaults.

Bond ETFs aren’t like individual bonds, though. They don’t mature so there’s no guarantee you’ll get all your money back no matter how long you hold them.

Fortunately, today, the prices of these ETFs are close to the lowest they’ve ever been, so you’d be buying them low. That doesn’t mean they can’t go lower if interest rates keep going up, but I think they offer great value—yields in the 5% to 7% percent range and with the opportunity to make additional returns if rates go back down in the future.

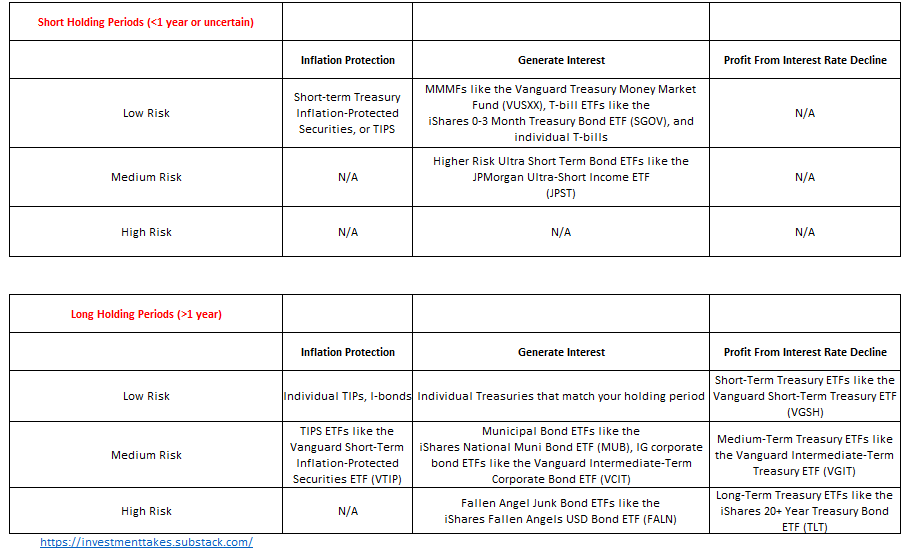

There are literally thousands of different bonds and hundreds of different bond funds out there, but most investors can meet their investment objectives with just a handful of choices.

This table which includes a selection of what I think are the bond investments that satisfy most investor’s needs. In the sections that follow, I’ll describe each option more thoroughly.

Short Holding Periods (<1 year or uncertain)

If you have a short-term holding period of one year or less (or you don’t know how long your holding period is going to be), you want to stick with safe bonds whose prices don’t fluctuate much, if at all.

Inflation Protection

For inflation-protection, I recommend short-term Treasury Inflation-Protected Securities, or TIPS. Individual TIPS are like any other individual Treasury bonds in that they have a maturity date on which you’ll get paid back in full—guaranteed.

But unlike conventional Treasuries, the return you get from TIPS is adjusted based on the inflation rate. If inflation is 7%, the government will adjust your principal upwards by the same amount. On top of that, you get an extra payment, which is known as the “real interest rate.”

That means when you buy TIPS, you are guaranteed to maintain your purchasing power plus a little more—as long as the real interest rate is positive like it is now.

You can buy short-term TIPS through most brokers.

Generate Interest

If you want to keep your cash in a safe place without locking it in for a long time, but while still generating some yield—almost like a bank account—then consider money market mutual funds, Treasury bill ETFs, and individual Treasury bills.

My top choice in this category is the iShares 0-3 Month Treasury Bond ETF (SGOV), but you absolutely can’t go wrong with the Vanguard Treasury Money Market Fund (VUSXX) either.

You can invest any amount of money you want into SGOV, while VUSXX has a $3,000 investment minimum.

One advantage of SGOV is it invests exclusively in T-bills. The income from T-bills—like the income from all bonds issued by the federal government— is exempt from state and local taxes.

VUSXX invests about two-thirds of its portfolio in government-issued bonds, while it invests the other third in repurchase agreements (which are super safe, but don’t get the same tax benefit).

Individual T-bills are another great option in this category. They’re more of a hassle to buy than either SGOV or VUSXX, but if you’re willing to put in the extra work, you might be able to eke out a slightly higher return by going this route since you wouldn’t have to pay a fee to a fund manager.

If you want even higher returns and you’re willing to take more risk, consider the JPMorgan Ultra-Short Income ETF (JPST). Unlike SGOV and VUSXX, which invest in U.S. government bonds and other risk-free investments, JPST invests in the short-term debt of other issuers, like corporations.

In the five years it’s been around, this has been a well-managed fund that’s earned an extra two or three percentage points of return versus SGOV and VUSXX. If you think that type of gain is worth it for the higher credit risk, this is an option.

Profit From An Interest Rate Decline

Short-term bonds aren’t very sensitive to changes in interest rates, so these aren’t what you want to invest in if you are looking to profit from bond price appreciation due to a decline in interest rates.

Long Holding Periods (>1 year)

If you have a holding period of more than one year, interest rate risk starts to become more of a factor. Fortunately, there are ways to neutralize that risk (if that’s what you want).

Inflation Protection

Treasury Inflation-Protected Securities (TIPS) offer great inflation protection over both short-term and long-term holding periods (see the section above for a description of what they are).

When you buy them with the intention of holding them for longer than a year, make sure to buy the TIPS with a maturity that matches your holding period. That will keep you from having to worry about what happens with interest rates.

For holding periods of longer than a year, Series I Savings Bonds become an option as well. iBonds are similar to TIPS, but have some key differences.

Like TIPS, iBonds’ returns are based on the inflation rate. But unlike TIPS, these bonds can’t be sold to another investor. Rather, you can redeem them with the Treasury, but only one year after you buy them. And if you redeem them before five years, you lose the last three months of interest.

One big benefit of iBonds versus TIPS is you can defer paying taxes as long as you hold them. With TIPS, you have to pay taxes on your interest and principal appreciation every year.

Because of the tax benefit, I prefer iBonds, but you are limited to purchasing $10,000 to $15,000 per year worth of these bonds, so for larger amounts, TIPS are the best option.

If you want to buy TIPS without wading directly into the bond market, you can consider an ETF like the Vanguard Short-Term Inflation-Protected Securities ETF (VTIP). This ETF holds TIPS with an average maturity of 2.5 years, so it does have a noticeable amount of interest rate risk.

Generate Interest

The safest way to generate interest on your money over a period of more than one year is to buy individual Treasuries with maturities that match your holding period.

If you have a two-year holding period, buy a two-year Treasury. The price of your bond might go up and down over the course of those two years, but once the bond matures, you will get all of your money back. Plus, for as long as you hold the bond, you’ll get paid interest on your money every six months.

Today, Treasuries are offering interest rates of anywhere from 4% to 4.5% percent with no credit risk, which is great. But what if you want even higher interest rates, in the 5% to 7% percent range?

Well, then you can consider municipal bonds and investment grade corporate bonds. These bonds aren’t super high risk, but unlike Treasuries, they do have some credit risk—so diversification is critical when buying them. That’s why I suggest looking at ETFs if you are going to invest in these types of bonds.

Munis are bonds issued by local and state governments. They are considered riskier than Treasuries, but still extremely safe, especially if you buy a diversified basket of them using an ETF. Even in 2020, when state and local governments were really strapped for cash because of the pandemic, they received support from the federal government and so their default rates stayed super low.

Munis are awesome because for most of them, you don’t have to pay federal taxes on the income you receive. And if you buy munis issued by the state you live in, a lot of times, you don’t have to pay state taxes either. This makes them great for taxable investment accounts, but you’re better off in Treasuries or corporate bonds if you are investing in a tax deferred account like a 401k or IRA.

The most straightforward, diversified muni ETF is iShares National Muni Bond ETF (MUB). This is yielding 3.7% right now, but remember, you don’t have to pay federal taxes on the income, so the taxable equivalent yield for people in the highest income tax bracket is around 5.8%. In other words, if you bought a normal bond where you have to pay federal taxes, it would have to pay more than 5.8% for it to give you a higher after-tax return than MUB.

Of course, this has to be adjusted based on your tax bracket and if you are buying these investments in a tax deferred account like a 401k or IRA, the tax benefit doesn’t matter. Use this formula to adjust a muni yield into a taxable equivalent yield:

Taxable Equivalent Yield = Tax-Free Municipal Bond Yield/(1 -Tax Rate)

In general, the higher your tax bracket, the more attractive munis are.

But what if you’re in a mid-to-low tax bracket or you’re investing in a tax deferred retirement account?

In that case, corporate bonds might be a better option for you. Investment-grade corporate bonds, which are bonds issued by the highest quality corporations, have historically been pretty safe.

A great ETF for investment grade corporate bond exposure is the Vanguard Intermediate-Term Corporate Bond ETF (VCIT), which is currently yielding around 6%.

If you want to take more risk for a higher yield, then you might want to consider a fallen angel corporate bond ETF like the iShares Fallen Angels USD Bond ETF (FALN). Junk bonds, or corporate bonds with low credit ratings, are usually extremely risky, and have high default rates.

But FALN only invests in bonds that previously had good, investment-grade credit ratings that were subsequently downgraded to sub-investment-grade, or junk bond, territory. These are known as fallen angels.

These are the highest quality of junk bonds, and they have lower default rates than the overall junk bond category. Companies whose bonds have become fallen angels also have an incentive to get those bonds upgraded back to investment grade. In cases they are successful, that results in higher prices for those bonds—and an ETF like FALN would benefit from that.

The fallen angels strategy has delivered some pretty nice returns over the past couple of decades, even doing better than stocks over some long periods. FALN is currently yielding more than 8%.

Consider this ETF if you want to stretch for yield and have a high risk tolerance. For safer exposure to corporate bonds, stick with VCIT.

Profit From An Interest Rate Decline

Prices for most bonds will fluctuate based on movements in interest rates. Even the bonds with the shortest maturities fluctuate in price—though those movements might be so small you hardly notice them.

But as the payments you receive from a bond move further out into the future, that bond’s price becomes increasingly sensitive to interest rate fluctuations. That’s what I’ve been referred to as “interest rate risk.”

Interest rate risk cuts both ways. It can be a good thing if rates drop and the price of your bond goes up, or it can be a bad thing if rates spike and the price of your bond declines.

Some of the bonds and bond funds I’ve mentioned up until now, including individual Treasuries, MUB and VCIT, will benefit if interest rates go down. In addition to receiving interest payments, you’ll see the value of those investments go up.

But say that your primary investment objective is not to collect interest payments, but to capture any potential price appreciation from a decline in interest rates. If that’s your objective, then you might as well do away with credit risk altogether and only focus on interest rate risk.

At the same time, you might as well do away with individual bonds and only focus on bond ETFs, which are easier to trade.

If interest rate sensitivity is what you want, then I would suggest taking a look at the Vanguard Short-Term Treasury ETF (VGSH), the Vanguard Intermediate-Term Treasury ETF (VGIT) and the iShares 20+ Year Treasury Bond ETF (TLT).

It’s worth noting that even though these ETFs are great options for getting exposure to interest rate changes, they also pay interest. Today, each of those funds is yielding more than 4%; so you can generate some nice interest while you wait for rates to (hopefully) move down in the future.

Of the three ETFs, TLT is the most interest rate sensitive, followed by VGIT and VGSH. If you want the maximum upside (and downside) from changes in interest rates, go with TLT. If you still want exposure to interest rate movements but don’t want to take as much risk, consider VGSH and VGIT.

TLT, in particular, makes for a good hedge against downside economic shocks. If we get something that comes completely out of left field—another pandemic, a global war, whatever it may be— there is a very good chance Treasuries are going to go up in price. So having that downside protection from long-term Treasuries is a nice benefit.

Very good article!

Insightful and valuable.

Many thanks Sumit!

Sumit, this is a great article you've written!

Easy to read and very practical. Articles like this are well worth the money to read!

Thank you so much!