Data Analytics Showdown: Palantir vs Snowflake

Data Analytics Showdown: Palantir vs Snowflake

Which stock is the better buy?

Palantir (PLTR) is one of those companies you might have heard of, but aren’t exactly sure what they do. Several years ago, the company was in the news quite a bit for its role in aiding the CIA in the war on terror, and more controversially, helping the NSA to snoop on ordinary Americans (the company denies it).

Palantir develops software for data analysis. It is used for data modeling, data summarization and data visualization. Here’s an excerpt from an old blog piece in which the company explained what it does:

“You could say that we help summarize large data sets, in the sense that we have to provide the analyst with a rich library of techniques and algorithms. You could also say that we do visualization, in the sense that we have to provide the analyst with a set of interesting and informative ways of visualizing their data. We do both of these things, and we have to be creative and solve hard problems in order to add value in these areas. But we do a lot more than that.

Probably the most central hard problem that we address in trying to enable the analyst is data modeling, the process of figuring out what data types are relevant to a domain, defining what they represent in the world, and deciding how to represent them in the system.”

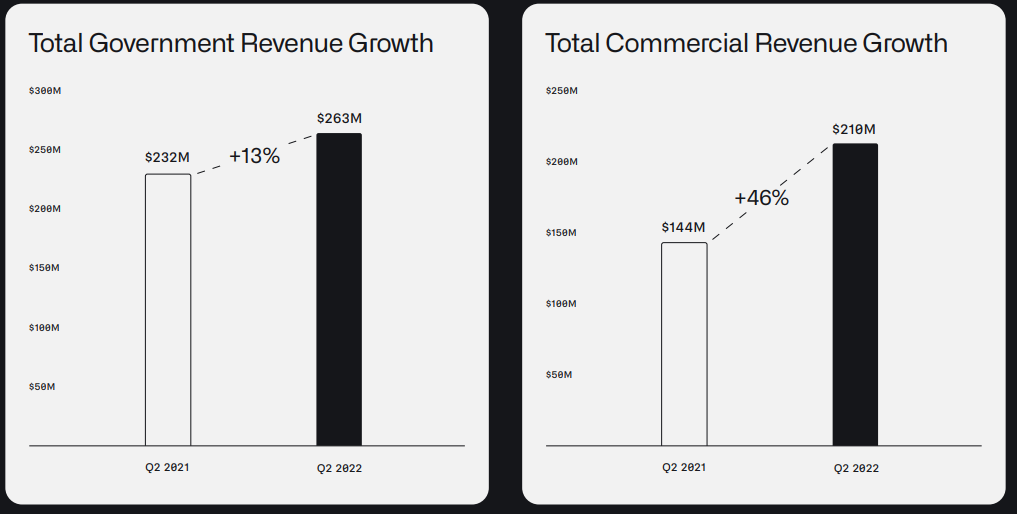

There are a few important things to know about this company. First, it generates the majority of its revenues from government customers, particularly the U.S. government. Selling to governments can be lucrative, but it isn’t a recipe for consistently high growth. That’s why Palantir has been trying to expand by selling its software to businesses.

Palantir’s challenge is getting companies to buy such a complicated piece of software. From what I’ve gathered, this isn’t software that’s easy to use or understand. It’s also extremely expensive.

That leads to long sales cycles, high sales and marketing expenses, and often the need for more customization and development on the part of Palantir to enable the software to fit different use cases.

In other words, the software isn’t as scalable as other types of software.

Analysts at Deutsche Bank echoed this sentiment in their downgrade of the stock following weak second quarter results:

“We have always been skeptical around the long-term economics of the business, and ultimately the extent to which Palantir is a true Software company vs. a highly skilled professional services firm with reusable intellectual property.”

Indeed, it is quite concerning that this company has been unprofitable since it was founded 19 years ago. Recently, the firm has been reporting positive free cash flow, but that’s largely because of the huge amount of stock-based compensation they use to pay employees.

That’s not that unusual in the software space, but the amount of stock-based compensation at Palantir is exceptionally high compared to others.

I’m also skeptical about how much growth this company has really seen in recent years. Palantir points to the fact that revenues are up from around $600 million in 2018 to around $2 billion this year, but there were reports that as a private company, Palantir was generating revenues of $1.7 billion as far back as 2015.

If that’s true, the company has hardly grown in the past seven years.

It’s pretty obvious that I don’t own Palantir. But the proliferation of data and the need to harness that data to stay competitive is only growing. Data analysis is a massive opportunity and there is one company in particular that is positioned perfectly to capitalize on it.

The Data Cloud

I don’t think there’s a better stock out there for exposure to data analytics than Snowflake (SNOW). Snowflake’s main offering is a cloud-based data warehouse.

A data warehouse is a type of database that is optimized for analytics.

Companies have troves of data—things like operational data and customer data—that they want to analyze to improve their businesses. They take that data, put it in a data warehouse like Snowflake and then do analysis on that data when they need to.

In the past, this was a very difficult thing to do. To run these types of analysis, you need an enormous amount of compute and storage resources— something that only a few of the biggest companies could afford.

Now with the cloud, anyone can access compute and storage resources on demand through Amazon’s AWS, Microsoft’s Azure, and Alphabet’s GCP. Snowflake takes advantage of that. Its data warehouse is built on top of those cloud providers.

It’s a total game changer and makes data analytics much more accessible to any company.

More recently, Snowflake has been expanding its offerings outside of its original data warehouse product, including tools to build data pipelines and run more advanced machine learning workloads.

And what I’m really excited about is Snowflake’s data sharing capabilities. Now Snowflake customers can share data between each other in a secure manner. They’ve even opened up a data marketplace, where companies can sell data to other companies who can then go and use that data for their own purposes.

That’s pretty cool and could be a competitive advantage for the company, as it increases the value proposition of being a Snowflake customer.

From what I understand, Snowflake is considered to be one of the top, if not the top cloud-based data warehouse on the market. The big three cloud infrastructure providers, AWS, Azure and GCP also have their own data warehouses.

Google’s BigQuery data warehouse is talked about highly, but overall, Snowflake is largely seen as best of breed today.

When Snowflake comes up, a lot of people talk about competition from Databricks as well. Databricks provides software for really advanced analytics like machine learning.

At least today, the two companies don’t usually compete head to head. Databricks is for more advanced analytics, while Snowflake is for more common types of business analytics— though the two are increasingly encroaching on each other’s turf as time goes on.

In any case, these are huge markets, so there’s more than enough room for multiple players. Snowflake will have to continue to develop its technology to ensure that it maintains its leadership position against not only Databricks, but all of these other massive companies with deep pockets.

I like Snowflake a lot and am overweight the stock. The biggest risk for the stock, aside from potential competition in the future, is the valuation. This was the biggest software IPO of all time in 2020; there was a ton of hype around it.

That’s understandable given how much potential this company has, but since that IPO, valuation has been a drag. On its first day of trading in September 2020, Snowflake closed at $254. Today, almost two years later, it’s $154, even though revenues have triples in that time frame.

Currently, the stock is trading at around 14.8 next year’s revenues, which is expensive, but much cheaper than it was a year or two ago.

Snowflake will have to keep executing flawlessly to justify this valuation. If it does—and that’s a big if— then at this price, the stock could be a big winner. Each investor has to make their own decision about whether the stock can meet or exceed the expectations embedded in the current stock price.

Like I said, I own it and will probably hold for a long time regardless of what happens to the stock in the short-term.

We’ll see what happens.