Starbucks & Lululemon Plummet: Game Over or Opportunity?

The stocks of Starbucks, Ulta Beauty and Lululemon are plunging. Here's why.

What do Starbucks, Lululemon, and Ulta Beauty have in common?

You might be thinking that they’re all brands popular with women— but that’s not the only similarity that they share.

The stocks of each of these companies has been plunging recently.

Shares of Starbucks have lost nearly a fifth of their value this year, while Ulta and Lulu have dropped by more than a third in just the past two months.

What’s going on? Is this a signal about the health of the economy? Or is this an opportunity to buy some of these stocks on sale?

Full disclosure: I bought one of these stocks today, and I fully hedged the position, giving me a maximum loss of 10% with potential upside of 50%.

I’ll tell you more about that trade soon, but first, let’s talk a little bit about Starbucks.

You know, it’s funny—Starbucks has a reputation for being this overpriced place where women go to drink their pumpkin spice lattes. But in reality, more men frequent Starbucks than women.

But that’s beside the point; the important thing is that Starbucks is facing an extremely tough time right now.

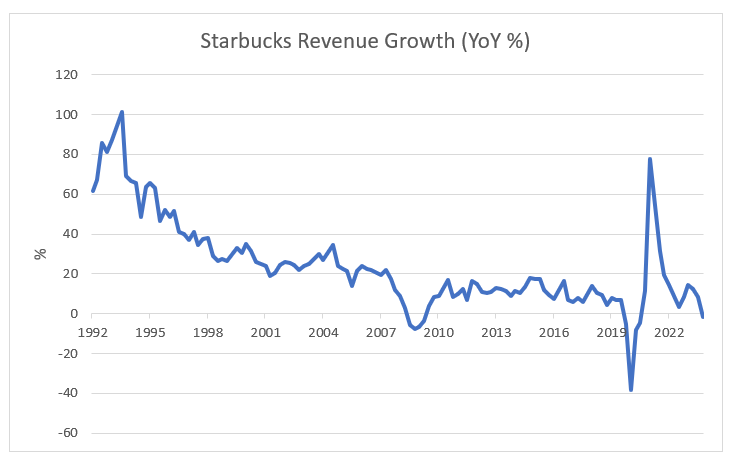

The company reported its latest quarterly financial results a few weeks ago and there’s no sugar coating it—it was a disaster.

Revenues were down 2% from a year ago, transactions were down by 6%, and profits were down by 14%.

The company blamed a host of factors for the dismal results— everything from severe weather to boycotts in the Middle East to a deteriorating economy.

Now, weather is obviously not going to be a drag on Starbucks over the long-term, and I don’t think boycotts related to the situation in Gaza will have a lasting impact either.

What’s more uncertain, though, is the demand for Starbucks from what the company calls the “occasional customer.”

These are the people who don’t visit Starbucks regularly, but might swing by the store to grab a drink or some food once in a while.

Starbucks executives say that these occasional customers have been stingier about opening their wallets because of the economic pressures they’re facing.

But some investors worry that the company has deeper rooted problems. They’re concerned that Starbucks has lost its way, that its drinks are too expensive, and that visiting its stores is a lousy experience—all of which are obviously bad, not just for attracting occasional customers, but for retaining the loyalty of regular customers as well.

Howard Schultz, the former CEO of Starbucks, recently suggested that the company has fallen from grace because it’s been focused on making money rather than providing an appealing experience for consumers.

Starbucks needs to “focus on being experiential, not transactional,” he wrote on LinkedIn.

Starbucks’ current management team seems to be listening. In the latest earnings conference call, CEO Laxman Narasimhan, outlined quite a few things that his company is doing to try to right the ship.

For instance, Starbucks is working to improve its app and in-store experience by making it easier and faster to place and receive orders.

It’s also aiming to roll out new products more quickly. The company highlighted zero calorie energy beverages and plant-based drinks as areas where it has been innovating.

Starbucks is also testing a program where it serves customers overnight between 5:00 p.m. and 5:00 a.m., hours when its stores are typically closed.

So, those are all things Starbucks is doing to improve the customer experience and potentially reinvigorate growth.

But it also plans to boost growth by opening new locations.

A lot of people think of Starbucks as being everywhere already. In some cities, you see a Starbucks on every block, but if you look outside the U.S., Starbucks’ presence is much smaller.

That’s why the company believes that it has a lot of opportunity to grow by expanding internationally.

You might be surprised to hear that Starbucks plans to open eight new stores a day through the end of the decade, increasing its store count to 55,000 by 2030 from 38,000 today.

Most of that growth is taking place in emerging markets like India, Indonesia and China.

In its latest earnings conference call, Starbucks’ management team made it a point to mention that coffee consumption in China is still very low relative to other countries at 13 cups per person per year.

When you consider that per capita consumption in Japan is 280 cups and in the U.S. it’s 380 cups, that leaves a lot of potential upside for coffee consumption in China.

That being said, the Chinese market is extremely competitive. Starbucks’ same store sales in China were down a whopping 11% year-over-year in the latest quarter, a decline the company attributed to weak economic growth and fierce competition from cheaper coffee retailers in the country.

Still, the company remains optimistic about the growth opportunity in China, as well as other international markets. It thinks it can continue to stand apart from the competition by offering consumers premium drinks and a premium experience.

Time will tell if they are able to achieve that.

I don’t own any Starbucks in my portfolio today, but after the recent sell off, the stock has become a lot more attractive.

It’s trading at less than 20x forward earnings for the first time since 2018, which is well below its 10-year average P/E of 27.

For a company that has ambitions to grow earnings per share at a 15% or greater clip over the long term, that’s a pretty good value.

There looks like there could be some chart support around $71 or $72, so if it gets back down there, I might start building a position.

Okay, so that’s Starbucks. The next company I want to talk about is Ulta Beauty. If you’re not familiar with Ulta, it’s the largest specialty beauty retailer in the U.S.

They sell cosmetics, fragrances, skin care products, hair care products, and salon services.

They’ve grown extremely fast, from around 700 stores in 2014 to just under 1,400 stores today. Women, who are the predominant customer base of the company, love that Ulta is a one-stop shop for all of their beauty needs.

It’s what’s helped fuel the company’s growth and turned Ulta into a company valued at almost $20 billion.

But that growth seems to have hit a bump in the road recently.

In April, Ulta’s CEO David Kimbell revealed that sales growth at its stores had slowed down meaningfully compared to what it was at the end of last year.

He blamed higher credit card debt and student loan payments for the slowdown, but some analysts believe that there are bigger problems facing the company.

Wells Fargo, which has a sell rating on the stock, recently laid out a three-point bear case for Ulta.

The first issue is that Ulta is losing market share to Sephora, the company’s arch rival which is owned by LVMH, the luxury conglomerate best known for its Louis Vuitton brand.

Issue number two is the threat from e-commerce giant Amazon. Analysts at Wells Fargo say that Amazon has “doubled down” on the prestige beauty category by partnering with L’Oreal and Estee Lauder.

They say that as Amazon continues to make headway in that category, it’s going to bite into Ulta’s sales and force it to invest more heavily in its online presence, which will pressure its profit margins.

The third issue that Wells Fargo talks about is something that was supposed to help Ulta, but might actually be hurting it: its partnership with Target.

Starting in 2021, Ulta unveiled a “shop in shop” concept in which Ulta got its own section within Target stores. There are now 500 Target stores with these Ulta sections and the concern is that they could be cannibalizing Ulta’s own stores.

So, that’s the bear case for Ulta, but of course, not everyone is negative on the stock.

Analysts at JPMorgan have a buy on the stock with a $530 price target. They say the company operates in an attractive, growing industry and that it has a unique model of selling higher-end “prestige” makeup and skincare products together with more affordable “mass [market]” makeup and skincare products.

Personally, I don’t have a strong opinion on Ulta. I think the company has done a fantastic job executing and getting to where it is today, but can it continue to thrive in a crowded market with Sephora and Amazon breathing down its neck?

I don’t have convincing answer to that question, so even though the stock is trading at 14x estimated forward earnings, the lowest P/E since 2009, I’ll be sitting this one out.

That said, if you’re a fan of Ulta, maybe it’s worth taking a look at the stock.

Where I do have more conviction, though, is the next company I’m going to talk about: Lululemon.

Like Ulta, Lulu is a retailer. But unlike Ulta, it sells its own products—most notably, yoga pants, which LuluLemon founder Chip Wilson invented in the late 90’s.

Wilson and his company are credited with pioneering the modern athleisure clothing category. Annual sales have grown from around $1.5 billion ten years ago to almost $11 billion today.

But it hasn’t been all smooth sailing for Lulu. In its time as a public company, Lululemon has seen multiple, harrowing drops in its stock price as investors often wondered whether the company’s products were a fad, and whether competitors would eat its lunch.

We seem to be in the midst of another such drop today, with shares of Lulu moving straight down from a high of $479 on March 21 to less than $300 today.

The culprit was the company’s first quarter earnings report, which showed that sales of the company’s products weren’t growing as fast as analysts and investors had expected.

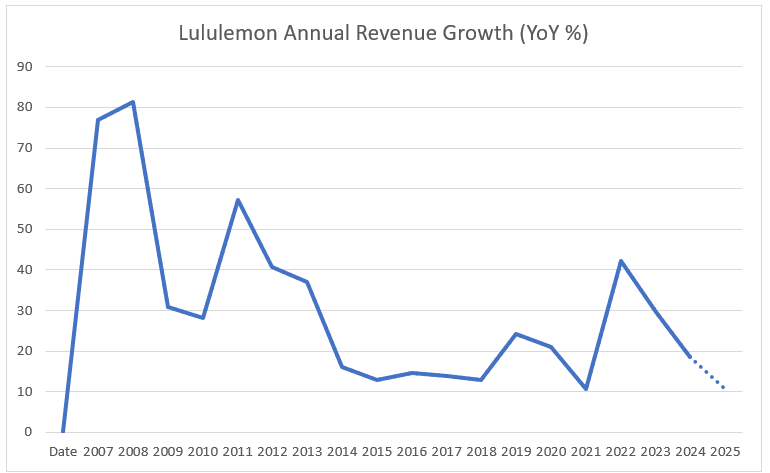

Lulu forecast revenues of $10.75 billion for the year, which is growth of around 11% compared to last year.

For context, Lulu grew revenues by almost 19% in 2023 and in its decade-and-a-half as a public company, it hasn’t grown by less than 10.6% in any year.

The fact that growth rates are forecast to drop towards the low end of the historical range might have spooked some investors and lent fuel to some of the bearish narratives surrounding the company.

Bears argue that fashion trends may be shifting away from athleisure, something that, if true, would be extremely negative for a brand that is hyper focused on the space.

There is also the worry that within athleisure, up-and-coming brands like Alo Yoga, Vuori, and FP Movement could be stealing market share from Lululemon.

To me, Lulu is an interesting company. I don’t have a ton of Lululemon products myself (I got a pair of Lulu joggers last Christmas, which I wear all the time— that’s about it).

But you don’t have to wear Lululemon yourself to know just how big and revolutionary this company has been when it comes to apparel.

Lululemon is synonymous with athleisure, and as long as people like to wear that type of clothing, they are going to be a big and profitable company.

Sure, there are competitors, but that’s to be expected in a fast-growing industry.

And Lulu isn’t just a sitting duck. The company is moving aggressively to expand outside of the areas it has traditionally dominated, into areas such as footwear, accessories, men’s clothing and internationally.

So, this is a case where I’m willing to bet that a category leader stays the leader. And with the stock trading at 20x forward earnings for the first time since 2017, I think it’s worth a look at these levels.

That said, Lulu is a highly volatile, risky stock. Fashion trends can be fickle; if the bears are right and athleisure is going out of style, maybe Lulu’s growth will be slower going forward, causing the stock valuation to compress further.

Given the risks, in addition to the stock, I bought at-the-money put options expiring in January. If you’re not familiar with options, puts go up in value when the stock price goes down.

So, by buying these puts, I’ve fully hedged my position as the put gains will offset the stock losses if the stock goes down.

The hedge isn’t free though. The puts with a $290 strike price, which is just below the current stock price, cost around $30 per share, or around 10%.

That $30 gets added to my stock purchase price of $295, bringing my effective buy price up to $325. If the stock is trading below that level when the puts expire in January, I will have lost money.

But my maximum loss is around 10%, no matter how low the stock goes.

On the other hand, if the stock goes up, I’ll capture a lot of the upside. Lulu was trading above $350 just two weeks ago and over $500 at the start of the year.

If the stock went back to its highs by January—which I’m not expecting, but you never know—I’d capture a more than 50% gain.

That’s pretty good potential upside for a fully hedged position.

Anyway, I’m not recommending anyone make this trade; this is just for educational purposes. My Lulu position represents about 2% of my portfolio— so it’s not a big position by any means— but I like the risk/reward here, especially with the puts.