Investing In Oil

Why oil investors made a ton of money even as oil prices fell.

(You’ll find the text version below this embedded video)

Something highly unusual has happened in the energy markets this year.

Even though crude oil prices are down since the start of the year, investors in oil have made a lot of money.

Take a look at the performance of WTI and Brent, the two most popular crude oil benchmarks—they’re down 6% and 2%, respectively.

Yet, United States Oil ETF (USO) and United States Brent Oil Fund (BNO)—two ETFs which track those benchmarks—are up by 16% and 21%.

That’s a huge difference.

To understand why this has happened, we need to go over a few key concepts related to commodities and financial markets.

The first thing to know is that investing in most commodities, including oil, isn’t straight forward.

Think about how you might go about investing in oil:

You go out into the market and buy barrels full of oil; you sit on them until their price goes up; and then you sell them for a nice profit.

That sounds easy enough, but it’s nearly impossible to do in practice. No one is going to sell you crude oil and even if you could buy it, you probably wouldn’t want to because the stuff is extremely toxic.

Oil just isn’t something that most people, or even most companies, can go out and purchase. The majority of the oil in the world is bought by refiners, who turn the raw crude oil into useable products like gasoline and diesel.

There are some professional oil trading firms that have the capability to buy barrels of oil for investing purposes, but those are few and far between.

For everyone else, the closest they can get to buying physical barrels of oil is buying oil futures contracts.

What Are Futures?

Futures contracts are standardized agreements to buy or sell an asset on some future date.

Here’s how they work. Say you’re a farmer and you just planted some wheat, but you’re worried that the price of wheat might go down before you can harvest and sell your crops.

You can enter into a contract with a buyer who agrees to purchase your wheat at a predetermined price on a future date. By doing this, you can sell your wheat at a predictable price and you’re protected from any potential price drops.

Meanwhile the buyer—who might be a cereal company or some other consumer of wheat— is protected from potential price increases.

That’s essentially how futures contracts work, except there’s no need for a specific buyer to make an arrangement with a specific seller. Futures contracts are standardized and traded on exchanges, so anyone can buy and sell them at any time.

The earliest futures contracts were used in the agriculture markets, but nowadays you can find futures on everything from stocks indices to bitcoin and, of course, oil.

Futures Prices

Now that we’ve discussed how futures contracts work, we can talk about how they are priced.

Say the current price of oil—also known as the spot price— is $80/barrel. What do you think the price of a barrel of oil delivered one month from now is worth? How about a year from now?

Well, it depends. In theory, a barrel of oil one month or one year from now should be worth more than a barrel of oil today.

That’s because there are costs associated with holding oil—storage costs, financing costs and insurance costs.

A refiner who needs oil in one month could either buy the oil today and pay all of those costs, or it could purchase futures contracts to guarantee delivery of the oil when it needs it.

If buying a futures contract is cheaper, then the refiner is better off doing that. If buying the oil today and storing it is cheaper, then it’s better off going that route.

In theory, this equivalency should keep the price of oil in the future in-line with the current spot price plus all the costs associated with storage.

That, in turn, should result in an upward sloping futures curve, where futures contracts for later months are priced higher than futures contracts for nearer months—a situation known as contango.

In theory, the oil futures curve should be in contango most of the time, but in reality, it’s not.

That’s because oil markets don’t always operate in a stable environment. Things can and do go haywire—like earlier this year, when Russia, the world’s second-largest crude oil exporter, invaded Ukraine.

Sanctions placed on Russia caused fears that the country’s oil supplies could be disrupted, leading to shortages.

As a result, oil buyers rushed to secure as much oil as they could get their hands on immediately. They didn’t want oil in the future—they wanted it today.

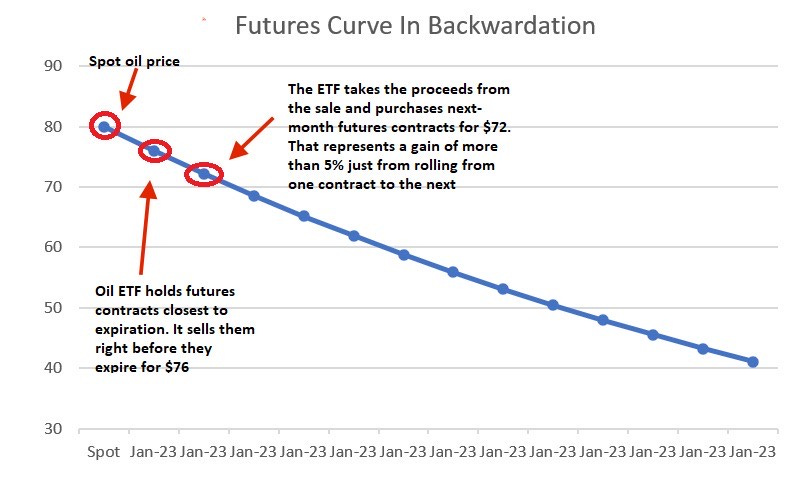

That pushed the price of spot and near month oil futures contracts much higher than later month futures contracts, a situation known as backwardation.

How Oil ETFs Work

With all that background, let’s come back to our two oil ETFs, USO and BNO. To get exposure to oil prices, these ETFs hold oil futures contracts—which, as I mentioned earlier, is the closest they can get to owning physical barrels of oil.

There are numerous oil futures contracts corresponding to every month of the year for the next decade, but oil ETFs usually hold near-month oil futures contracts, or those that guarantee delivery of oil in the near future (like one month from the current date).

They hold these futures because their price is closely tied to the spot price of oil.

As futures contracts reach expiration, their price tends to converge with the spot price of oil because at that point, real barrels of oil exchange hands.

Every futures contract represents the delivery of 1,000 barrels of oil. If you own futures contracts when they expire, then the seller of those contracts will deliver actual barrels of oil to you—a process that ensures that futures prices and spot prices stay linked together.

But because oil ETFs can’t take delivery of oil, they sell those contracts as they near expiration and buy the next available futures contract.

When the oil futures curve is in backwardation, these ETFs are essentially selling high and buying low.

That’s what they’ve done all year long, and it’s been a windfall for them because in 2022 we saw the steepest backwardation in oil market history. That means that spot and near month futures were priced way above later month futures.

That allowed oil ETFs to swap high priced contracts for low priced contracts, and that more than made up for the decline in the spot price of oil.

Who Oil ETFs Are For

Now does this mean you should run out and buy these ETFs? No. These are trading tools. If you have a strong view on oil prices or the shape of the oil futures curve, then you can use them for quick trades.

But even if you’re bullish on oil, these ETFs are not great long-term investments because when the oil futures curve is in contango—which it is around half the time—these ETFs have to sell low and buy high.

That ends up being a big drag on returns. As you can see, since the funds launched over a decade ago, both USO and BNO have lagged the returns for spot oil.

But if you are looking for an oil ETF that you can use for short-term trades, I’d recommend BNO over USO. Infrastructure bottlenecks at Cushing, Oklahoma—the delivery point for WTI—has resulted in several periods of really steep contango in the WTI futures curve, which as severely hurt USO’s returns.

On the other hand, if you’re looking for more of a buy-and-hold oil-related investment, an energy ETF like Energy Select Sector SPDR Fund (XLE) is a better bet.