Is the AI Earnings Boom an Illusion?

Famed short seller Jim Chanos argues that the AI capex boom is amplifying reported earnings. He has a point, but it's not the whole story.

S&P 500 earnings are on track to grow 21% this year, the fastest pace since 2021 and the second-fastest since 2010. The driver is overwhelmingly AI.

But famed short seller Jim Chanos thinks a meaningful chunk of that growth is mechanical, an artifact of how the AI capex boom flows through company financial statements.

He’s raising a question worth taking seriously: how much of what the market is celebrating is real, and how much is just how the accounting works during a buildout like this?

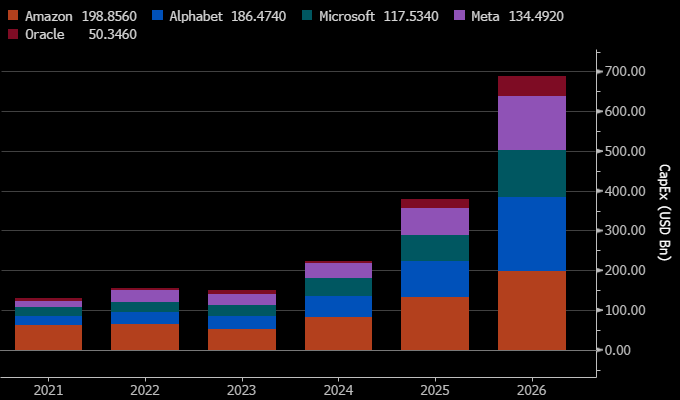

To understand his argument, here’s a bit of context. Spending on AI has been exploding. Microsoft, Google, Amazon, Oracle and Meta are on track to spend $700 billion or more on capital expenditures this year, most of it on AI data centers.

Companies across the supply chain have been big beneficiaries. Nvidia is the headline name, but it goes well beyond that. There’s Broadcom for custom chips and networking, Micron for memory, Vertiv for cooling, GE Vernova for the power equipment, Dell for the servers, on and on. Almost every company touching the AI buildout has been a big winner.

It hasn’t been a straight line up, though. Bears have called tops the whole way, saying the models would stall, Nvidia’s margins would collapse, GPUs would be obsolete in a year, or that big tech wouldn’t get an adequate return on their enormous spending.

Most of those calls have aged poorly. But Chanos’s argument is different, because he isn’t disputing that the tech is useful or that profits are rising. He’s saying the profit increase might not be what it seems.

Breaking Down the Mismatch

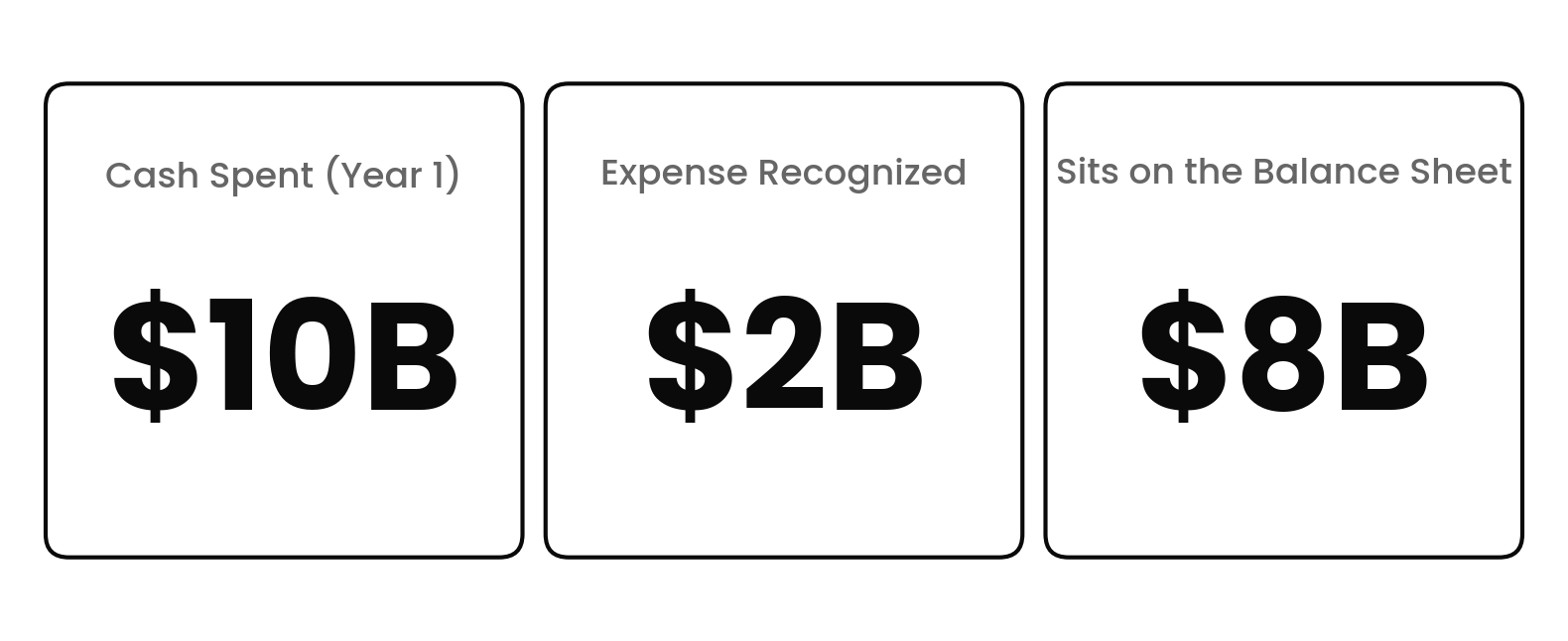

Imagine a big tech company like Google spends $10 billion on a data center. That spending leads to more revenues and profits for companies like Nvidia, Broadcom, Micron, and the whole supply chain that gets a piece of the expenditure.

Those companies recognize that revenue right away, and a huge chunk drops to their bottom line because profit margins in the space right now are sky high.

But for Google, that $10 billion doesn’t subtract completely from its income statement. It gets capitalized as an asset on the balance sheet and recognized over time, depreciated over the useful life of the chips and other infrastructure, which the big tech companies assume is five or six years.

So in year one, only a small fraction of that $10 billion shows up as an expense for Google. Maybe two billion. The rest sits on the balance sheet to be expensed over the following years.

So you have a big increase in profits for companies in the AI infrastructure supply chain, but not nearly as big a decrease for the spenders. That’s the accounting mismatch Chanos is talking about.

You can actually see it playing out in the financial statements. Despite spending aggressively on data centers, Meta, Amazon, Google, and Oracle are all reporting strong earnings growth.

You wouldn’t see the massive amounts they’re spending on their income statements, because most of it gets capitalized and recognized over time. Where you do see it is in free cash flow, which has compressed dramatically.

In the latest quarter, Meta reported $27 billion of net income but only $12 billion of free cash flow. Net income reflects the slow recognition of costs based on the accounting we just discussed. Free cash flow reflects the money actually going out the door right now. And right now, a lot more money is going out the door than the earnings number alone would suggest.

Why Bulls Aren’t Worried

So that’s the thesis. During these capital spending booms, profits pour into companies across the supply chain while costs to the buyers get deferred. That’s why corporate earnings can appear really strong during these periods.

Chanos argues that once the boom ends, the dynamic could reverse. Revenue dries up for the suppliers while the buyers are still depreciating the infrastructure they bought, and earnings get pulled lower as a result.

Of course, not everyone agrees with this view. Bulls argue there isn’t anything nefarious going on. This is literally how accounting works. When you build a long-lived asset, you spread the cost over its useful life.

And that makes sense. The accounting is trying to give you a sense of the true earnings of the business over time.

In fact, some bulls argue that the bears have it backwards. If the AI chips and infrastructure being deployed today are still generating revenue seven or eight years from now, then the five-to-six-year depreciation schedules big tech companies are using might actually be too aggressive.

In that case, the accounting is understating long-run earnings power, not overstating it. There’s evidence for this view. Nvidia’s older chips are holding their value much better than many had predicted.

The company’s Hopper chips, which started shipping in 2022, are still in heavy demand in 2026, with companies running them in production alongside the latest Blackwell chips.

So from that perspective, the timing question of when costs hit the income statement versus when supplier revenue does isn’t necessarily as alarming as it might look.

The Other Bear Argument

Bears argue accounting isn’t the only thing inflating earnings. They have a second concern, totally separate from how costs get recognized, about whether the money flowing through all of this is even real.

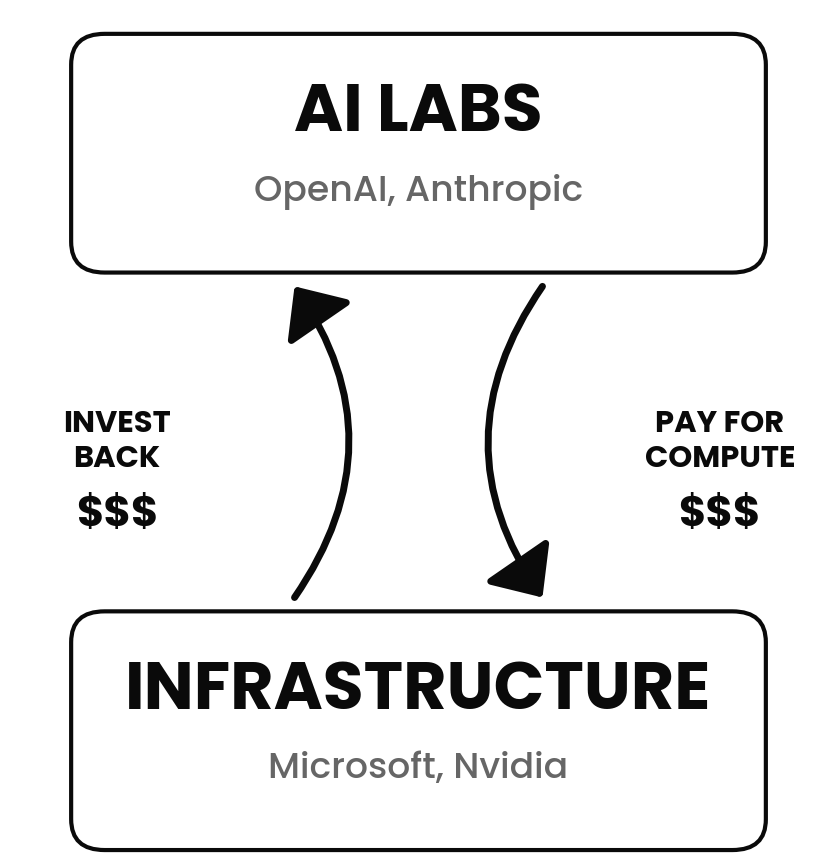

This is the whole circular financing idea. Sure, OpenAI and Anthropic are spending big money on AI infrastructure, the bears say. But they themselves are being funded by the companies building the AI infrastructure, and that’s not sustainable.

Here’s what they mean. Let’s say OpenAI spends $5 billion on compute from Microsoft to train and run its AI models. That’s real revenue for Microsoft, which uses some of it to buy more Nvidia chips. That’s real revenue for Nvidia too.

But then, using their cash, Microsoft and Nvidia turn around and invest billions of dollars back into OpenAI. OpenAI uses that fresh money to spend even more on compute and chips from Microsoft and Nvidia, boosting their revenues and profits. Those companies then reinvest more in OpenAI.

Each loop generates revenue and earnings, but it’s the same dollars circulating between a handful of companies.

The bulls’ counter is that the loop isn’t really a loop, because real outside money is pouring in. OpenAI and Anthropic are generating tens of billions in annualized revenue from actual paying customers, and ChatGPT and Claude are growing faster than basically any products in history.

So yes, some dollars are getting recycled between a handful of companies right now. But at the rate end-user revenue is growing, OpenAI and Anthropic will become self-sustaining well before the cycle breaks. Once they do, the circular element disappears, and all the money for AI starts coming from consumers and businesses who value the products.

What Matters Long Term

If we zoom out, both bear arguments are really pointing at the same thing. The accounting mismatch and the circular financing are two different ways earnings can get amplified during a capex boom, and both would work in reverse if spending slows.

But whether either one actually matters in the long run comes down to what happens to actual end demand for AI. If consumers and businesses keep spending more on the technology, then the recycled dollars get displaced by real outside revenue, the depreciating infrastructure stays productive, and today’s earnings might even understate the long-run picture.

If they don’t, the supply chain takes a much bigger hit than the underlying drop in demand alone would suggest, because both amplification effects unwind at the same time.

My Take

As time goes on, fewer people are questioning the usefulness or groundbreaking nature of AI itself. It’s more about whether the stock prices and the earnings being reported by tech companies truly reflect what’s happening underneath.

I’m certainly not an AI bear. I think the tech is revolutionary and I’m invested in several AI companies outside of my index funds. And I don’t suggest anyone run out and make drastic changes to their portfolios based on any of this. People have been calling this a bubble for over three years, and anyone who has fought the trend has been steamrolled.

But it’s worth examining the risks and understanding the dynamics. Some real portion of the earnings growth being celebrated right now is a mechanical effect of the nature of the infrastructure buildout.