Should Short Selling Be Banned?

The CEO of America's largest bank seems to think so.

“If someone is doing anything wrong, people are in collusion or people are going short and then making a tweet about a bank, they should go after them—and vigorously—and they should be punished to the fullest extent the law allows.”

That’s what Jamie Dimon, CEO of JPMorgan Chase, America’s largest bank, told Bloomberg on May 11.

His comments came a few days after the American Banker Association urged the SEC to investigate short sales against bank stocks. Meanwhile, many others are calling for an outright ban on short sales.

What are all these people talking about?

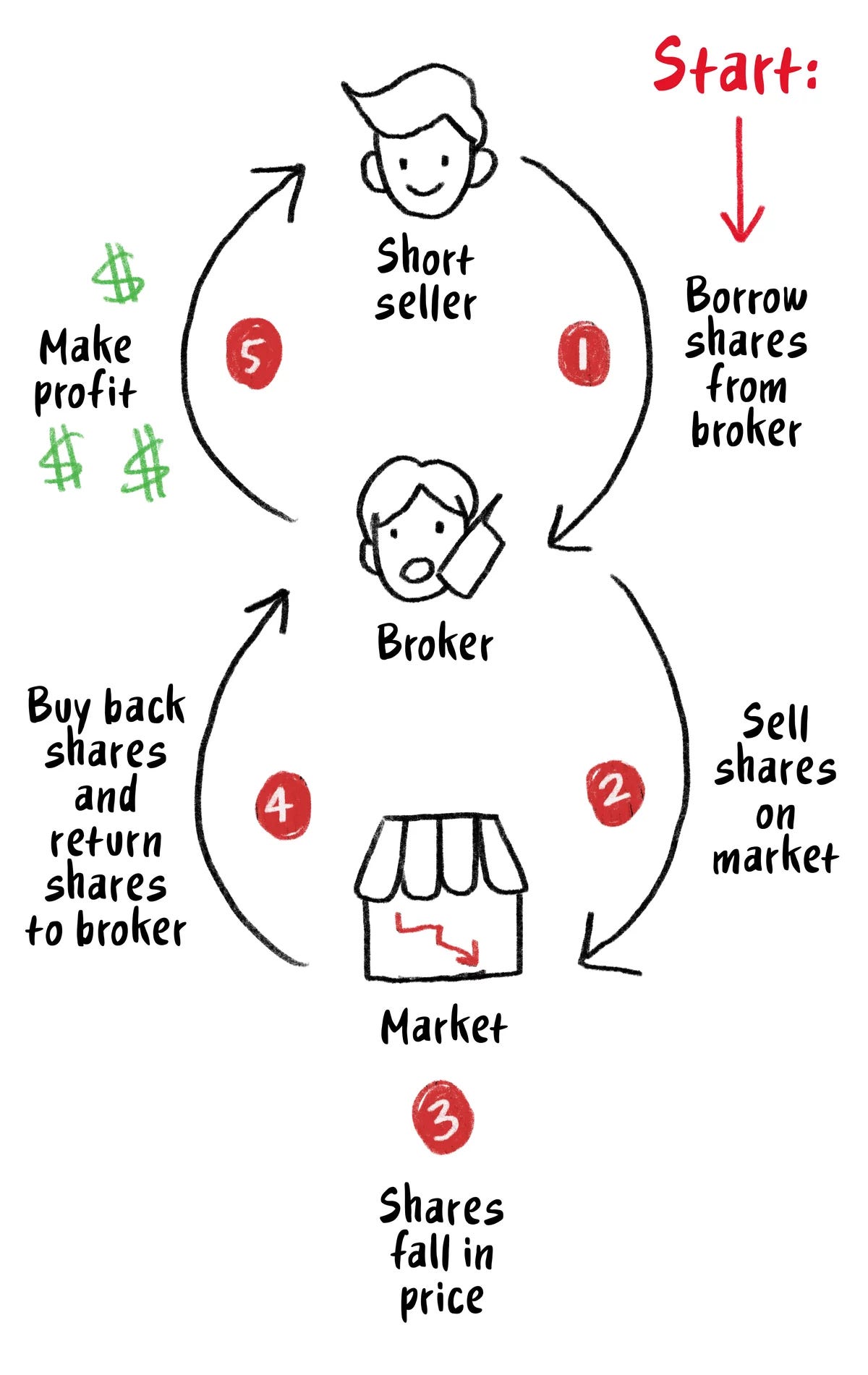

Well, they’re talking about short selling—an investment strategy for profiting when a stock goes down.

In a short sale, someone borrows a stock from another investor, immediately sells the stock on the open market, and then later repurchases the stock and returns it to the investor they borrowed it from.

If the short seller is able to repurchase the stock at a lower price than they sold it for, they profit.

What Jamie Dimon and others are concerned about is that short selling may be exacerbating the crisis at regional banks.

How is that possible? Well, the banking business model is dependent on confidence. Banks take money in in the form of deposits and they lend money out in the form of loans and other investments.

This model works well when depositors are confident that their money is safe. When that’s the case, banking is like magic: depositors get on-demand access to their money, while businesses, homebuyers and others who need to borrow money are able to do so.

It's a win-win-win and it's an engine for economic growth as it helps channel savings into productive investments.

But the model begins to fall apart when confidence in a bank is shaken. Banks only keep a certain amount of cash on hand—not nearly enough to pay back all of their depositors at once.

A small number of depositors taking their money out of a bank is fine and is to be expected. But if all of a bank’s customers rushed to withdraw their money at once, that bank—which probably has most of the money tied up in assets like loans and bonds—wouldn’t be able to pay everyone back and it would collapse, just as we saw in the case of Silicon Valley Bank.

So anything that damages confidence in a bank puts the bank’s business model—and potentially its survival—at risk.

That’s where short selling comes in. As I mentioned earlier, in a short sale, stock is borrowed from an investor and immediately sold on the open market, pushing down the price of a stock.

What some critics of short selling are suggesting is that if there is a lot of short selling, that could drastically push the price of a bank’s stock down, damaging confidence in the bank and causing depositors to take their money out of the bank. If confidence in a bank is shaken enough, the bank could even go under.

Now, most people do agree that anything that hurts confidence in a bank can be damaging to that bank—and that includes a plunging stock price—but that raises the question: can short selling in and of itself cause a bank’s stock price to plunge?

Well, in 2008, during the heart of the financial crisis in the U.S., the Securities and Exchange Commission briefly banned short selling in 799 financial stocks. We’ve also seen short selling bans in other countries throughout the years.

By analyzing those periods when short selling was banned and comparing them to periods when it wasn’t banned, we can learn whether short selling was responsible for big stock price declines.

What the research ultimately shows is that short selling doesn’t lead to big stock price declines in and of itself.

When the SEC banned short selling in financial stocks in 2008, it didn’t stop those stocks from falling, and in fact, it had other negative, unintended consequences.

You see, while short selling sometimes gets a bad rap, it actually serves a useful purpose in the markets.

Short sellers make the stock market more liquid. The more people there are buying and selling stocks in the market, the easier and cheaper it is to trade.

Short sellers also help reduce volatility in the market. You know how I said that they borrow stock and then immediately sell it? Well, they have to eventually buy that stock back to return it to whoever they borrowed it from.

So if a stock goes down significantly, short sellers usually start to buy, putting a floor under the stock price.

Short sellers also help with price discovery. Their selling and buying provides information to the market, helping drive stock prices towards their true value.

And thirdly, short selling can be useful when it comes to managing risk. Some people use shorts to offset regular long positions they have elsewhere in their investment portfolios.

For example, they might own an ETF tied to the Nasdaq like the Invesco QQQ Trust (QQQ) and then short an individual stock like Apple to hedge or offset that long position.

When short selling in financial stocks was temporarily banned in the U.S. in 2008, all of these benefits that came from shorting disappeared.

Christopher Cox, who was Chairman of the SEC at the time of the short selling ban, later when on to say that he regretted instituting the ban and that the costs of the ban outweighed the benefits.

That said, just because short selling in and of itself isn’t a problem, it can be a problem when it encourages market manipulation.

If someone shorts a bank's stock and then puts out an unfounded rumor about that bank in order to send its stock price lower and profit from their short position, that’s a problem.

But of course, the issue there is the market manipulation—the spreading of a false rumor to influence the stock price—not the short selling itself.

You could imagine that someone could buy a stock the normal way, put out a false rumor that sends the price of the stock higher and then benefit from that.

In both cases, it's the false rumor that's the problem, not the investment strategy itself.