T-Bills Yielding 7%

This is where we’re seeing the biggest market impact from the debt ceiling drama in the U.S.

This is where we’re seeing the biggest market impact from the debt ceiling drama in the U.S.

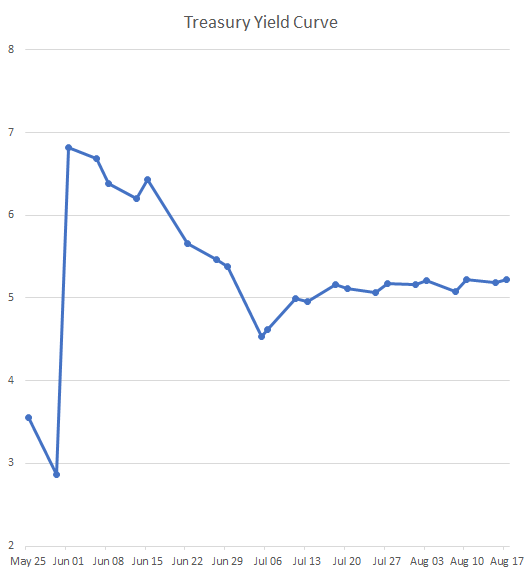

This is called the Treasury yield curve. It plots the interest rates that investors get for buying Treasuries of varying maturities (maturity being the date on which the government pays back the holder of the Treasury security).

As you can see, Treasury bills maturing in May have very low yields, while bills maturing in early June are yielding much more than those maturing several weeks later, like in July or August.

The May T-bills are yielding close to 3%; the June T-bills are yielding nearly 7%; and those maturing in July and August are yielding closer to 5%.

That’s a big difference and it’s a reflection of fear that the bills maturing in early June might not get paid back if the debt ceiling isn’t lifted by the date on which the Treasury Department runs out of money—which Treasury Secretary Janet Yellen estimates could be as early as June 1st.

Investors in T-bills are being prudent.

They know that the Treasury department has enough money to pay back bills maturing in May and that’s why they’re willing to accept much lower yields to invest in those.

They also know that the bills maturing in early June are at the highest risk of not getting paid back in the event of a default.

Why buy a T-bill maturing in June that would be the first to be impacted by a U.S. government default when you can buy bills maturing in July or August which have a much lower probability of being impacted because any default—if it happens—would probably only last a very short amount of time?

That’s the sentiment that the yield curve is reflecting.

If we don’t get a deal in the coming days and the probability of default continues to rise, then we’ll likely see the yield premium on those June T-bills continue to rise as well.

On the other hand, if we do get a deal to raise the debt ceiling or it starts to looks like we’ll get a deal, then the yield premium on the June T-bills will likely fall.

In other words, the yield curve is an indicator of how T-bill investors view the likelihood of default.

Another market-based indicator is the stock market. If default becomes likely, then naturally, you would expect stock market investors to sell.

But we haven’t seen much of that yet. The S&P 500 is right around where it’s been over the past few months—which isn’t that surprising.

Most people still think a deal is going to get done because we’ve seen this situation before, like in 2011 and 2013, and it’s always ended the same way—with a last minute deal.

So it’d be kind of silly to sell all your stocks based on something that seems to be a very low probability event. For T-bill investors it’s easier to cut down on risk—just buy T-bills maturing in May, July, or August instead of June.

For stock investors, it’s harder. Stocks are usually thought of as long-term assets and you don’t want to make drastic changes to your long-term investment plan over a very short-term, low probability risk.

That’s why we haven’t seen a lot of big moves in the stock market based on the debt ceiling situation.

But if that changes and we start to see big downside moves in the stock market, then it’s probably time to start worrying.