The Dollar's "Collapse" Is Good For America

Contrary to what the fearmongers would have you think, a diminished role for the dollar doesn’t necessarily spell doom for the U.S. economy

I’ve been hearing a lot of talk recently about how the U.S. dollar’s days are numbered and how that’s terrible for America.

But as strange as it may seem, a diminished role for the U.S. dollar could actually be good for America.

I know that sounds counter-intuitive, maybe even a little bit ridiculous, but hear me out.

First let’s break down what all this dollar talk is even about—without the fearmongering and politics that often surrounds this topic.

As you obviously know, the U.S. dollar is the currency of the United States.

That’s not going to change.

Within the U.S., we’re going to be using the dollar to make purchases, to measure the value of the things we buy and sell, and to store our savings— for a long time to come, probably forever.

But the dollar isn’t just used within the U.S. It has a very special role internationally as well.

Just like there’s a need for a currency for transactions, accounting and safe keeping inside of a country—there’s also a need for a currency to do all of those things internationally as well.

Say a company in Argentina wants to buy something from a company in Thailand. What currency are they going to use?

The Argentine company might want to make the purchase with Argentine pesos. But those pesos would only be useful to the Thai company if they were going to turn around and use them to buy something from Argentina.

But if it didn’t need anything from Argentina, what could it do?

The Thai company could hold onto those pesos and wait until they needed something from Argentina. But that day might never come and the whole time the Thai company would be worried that the value of those pesos would decline since Argentina has one of the highest inflation rates in the world.

Another thing it could do is exchange those pesos for its native currency, the Thai baht.

The company would just have to find someone who had baht and wanted pesos in exchange for them. But that’s a little bit of a challenge.

Given that Thailand and Argentina don’t do a whole lot of trade between them, there’s not a huge market for exchanging pesos into baht, so it might not be easy to find someone who has baht and wants pesos.

So rather than go through all of this, the Thai company could ask the Argentine company to pay it using another currency—one that has a stable, predictable value and one that’s easily convertible into all sorts of other currencies.

Maybe something like the U.S. dollar, the currency of the world’s largest economy.

So instead of pesos, the Thai company could ask to receive dollars. And it could either keep those dollars or convert them into any other currency that it needs.

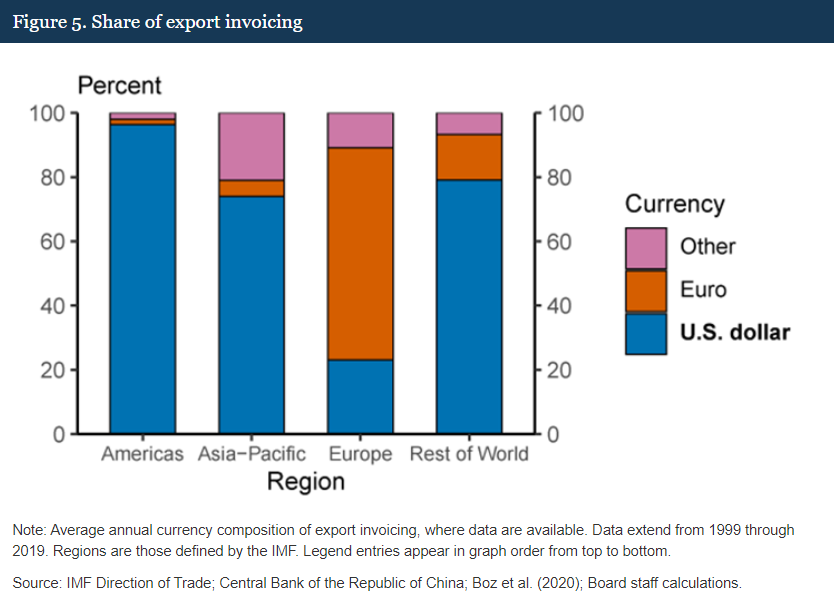

The dollar helps standardize trade between the dozens of countries in the world, each with their own currency. Outside of Europe, around 75% to 100% of international trade is conducted using dollars.

(Another benefit of using the dollar is it makes trade invoicing easier, since companies can just quote prices in dollars rather than in multiple currencies, all of which are fluctuating in value constantly)

The dollar isn’t just used for trade between countries.

Because of its strong reputation, people in other countries also sometimes use it to buy and sell things within their own countries or as a safe place to store their savings.

Nearly $1 trillion of physical U.S. dollars are held by foreigners, half of all U.S. banknotes in circulation.

That’s not all. Foreign governments—specifically, foreign central banks— also hold trillions of dollars. These are called foreign exchange reserves.

The central banks use these reserves to prop up their economies and their own currencies during times of economic turmoil. For instance, if the central bank of Thailand has reserves of dollars, then it can sell those dollars in exchange for baht to support the value of the baht if it needs to.

Some central banks also use foreign exchange reserves to manipulate the value of their currencies in order to influence imports and exports.

For instance, the Chinese government kept the Chinese renminbi (also known as the yuan) artificially low against the U.S. dollar for many years in order to make its exports cheaper and more attractive to consumers in the U.S. and elsewhere.

It did this by creating renminbi and then selling them in exchange for dollars—dollars which became a part of the Chinese central bank’s foreign exchange reserves.

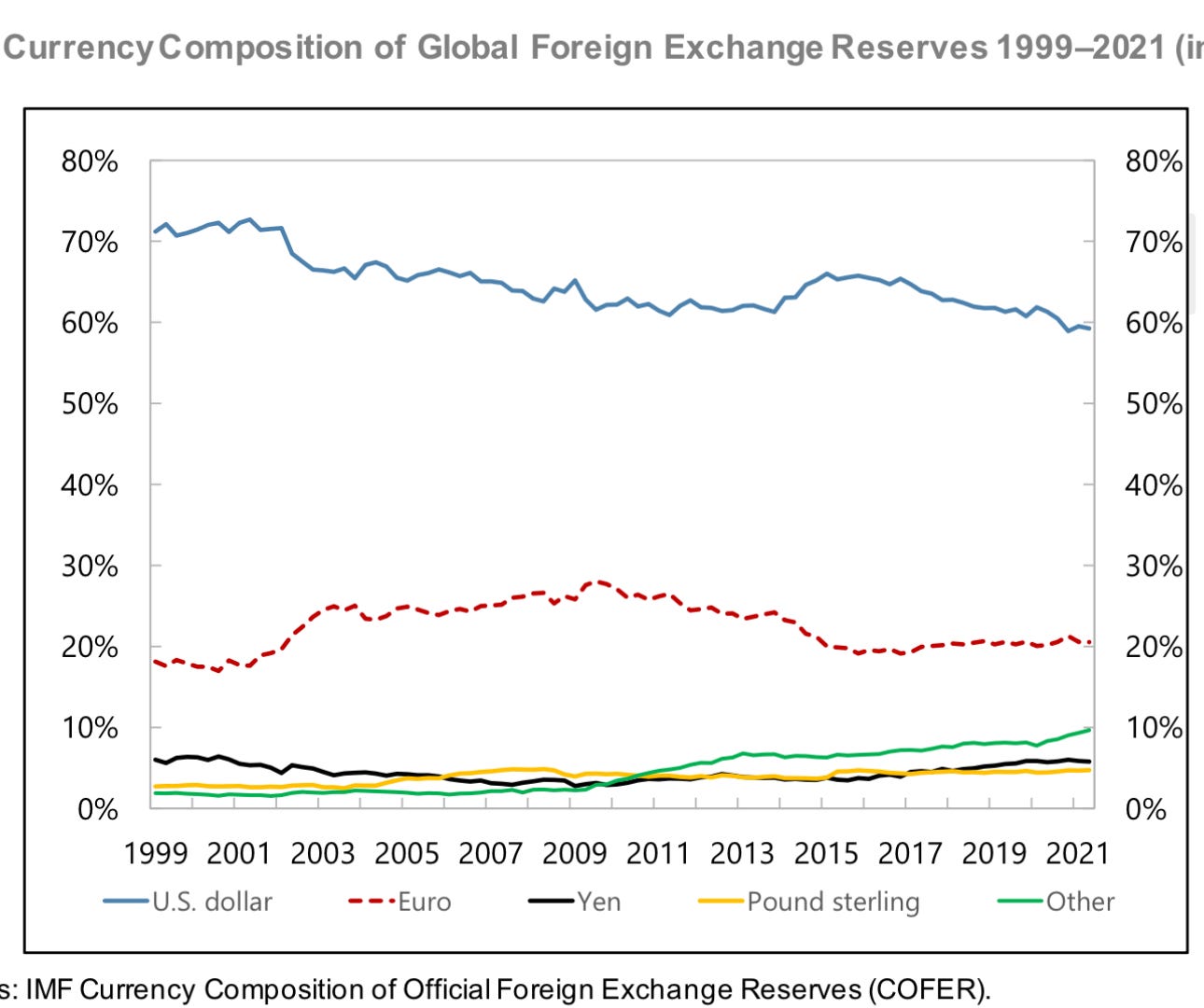

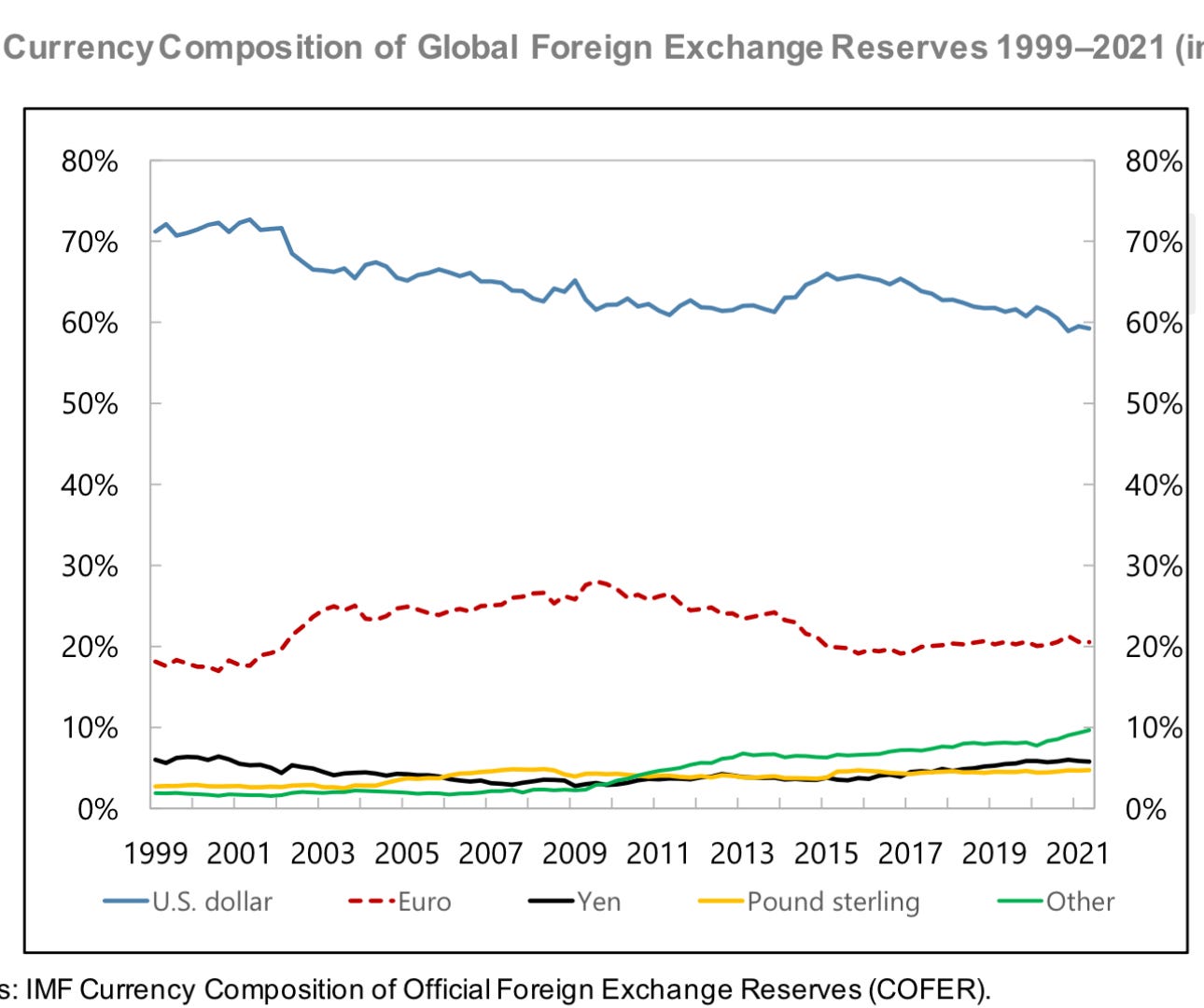

Today, the dollar is the most widely used currency within foreign exchange reserves, not just in China but across the world. And that’s why it’s called the world’s reserve currency.

The dollar makes up 59% of the world’s foreign exchange reserves, ahead of the euro, which has a share of 21%.

Now, so far, I’ve talked about how the dollar is the world’s top reserve currency and the top currency for international payments.

But does this actually benefit America in any way?

It does. When foreigners receive U.S. dollars, they usually use them to buy U.S. assets, putting upward pressure on their prices. This includes assets like stocks, corporate debt, and even real estate.

But the asset that most of the money goes into is U.S. Treasuries.

When foreign central banks hold dollar reserves, they usually keep them in the form of Treasury bonds.

The U.S. government issues Treasury bonds when it wants to borrow money, so foreigners who own these bonds are essentially helping to fund the government’s spending (about a third all Treasuries are held abroad).

This is something that’s helpful for the U.S. By being the world’s reserve currency, it increases demand for U.S. assets and puts downward pressure on U.S. interest rates (when Treasury bond prices go up, interest rates go down).

At the same time, because there’s so much demand for U.S. dollars internationally, it puts upward pressure on the dollar’s value compared to other currencies, making imports cheaper for U.S. consumers.

(To boil down what’s happening: other countries are trading goods and services for U.S. assets like Treasuries. And yes, since Treasuries represent government borrowing, the U.S. is effectively borrowing money from the rest of the world. As long as there is strong demand for dollars internationally, this dynamic can persist)

Here’s another benefit for the U.S.: having the dollar as the global reserve currency allows the country to punish its enemies through the financial system. Because dollars are so important when it comes to international commerce and finance, if the U.S. decides to cut off a person, a company or a country from getting their hands on dollars, it can be extremely damaging to them.

This is a weapon that the U.S. has used with increasing frequency in recent years. In 2022, the U.S. and its allies froze over $300 billion of Russia’s foreign exchange reserves—cutting in half the country’s international reserves in one fell swoop.

Sanctions are a powerful weapon that allow the U.S. to exert pressure on other countries without resorting to military force. The world’s reliance on the dollar helps enable that.

At this point, you’re probably thinking that having the dollar as the global reserve currency is only a good thing for the U.S. But there is a downside, and it’s this:

Because there is so much demand for U.S. dollars from foreigners, the dollar is much stronger than it would otherwise be. This creates a disadvantage for U.S. exporters when it comes to competing against foreign companies that operate in countries with cheaper currencies.

This headwind is strongest during times of economic uncertainty, when the dollar is in even greater demand because it’s considered a safe haven.

That’s the cost of having the world’s reserve currency—a less competitive export industry.

Some people even believe that the strong dollar has contributed to the decline of the U.S. manufacturing industry*.

If you believe that’s the case, then you might welcome a world in which there’s less demand for dollars and the currency is a little bit weaker because it could help the competitiveness of U.S. companies on the world market.

But let’s not get ahead of ourselves. While that’s something we could see in the future, the dollar’s dominance isn’t going to end anytime soon.

Like I said, the dollar is still the number one currency for foreign exchange reserves and for international payments.

The dollar’s share has been declining over the past couple of decades, but it’s been a slow grind lower, rather than a sharp drop**.

The main reason for that is there just hasn’t been a viable alternative to the dollar—a currency that’s widely accepted and recognized as a reliable medium of exchange and store of value.

The euro has many of the properties that are required to be a good international currency, but it’s still second to the dollar. Since it was created over two decades ago, its share of international payments and foreign exchange reserves has been close to unchanged.

A more formidable contender for the dollar’s crown might be the Chinese renminbi.

As the currency for the world’s second-largest economy, the renminbi has the potential to become a widely used currency internationally.

But so far, we haven’t seen the renminbi used very much outside of China. Currently, it makes up around 3% of foreign exchange reserves and it’s used in around 3% of international transactions.

The biggest thing holding the renminbi back is capital controls. The Chinese government limits how much of the renminbi can be bought and sold in order to maintain tight control over the currency and prevent big inflows and outflows of capital that could destabilize the Chinese economy.

But while these capital controls help the Chinese government implement its economic policies, they reduce the appeal of the renminbi for foreigners because they limit their ability to freely convert and transfer the currency.

If China ever relaxes its capital controls, then there’s a good chance that the renminbi will become much more dominant on the global scene given that China is currently the world’s second largest economy and one day will probably become the world’s largest.

So if that happens, the dollar’s international role will decline further.

But like I said earlier, contrary to what the fearmongers would have you think, a diminished role for the dollar doesn’t necessarily spell doom for the U.S. economy, and in fact, could come with some benefits.

The bottom line is this: the dollar’s dominant international role is overhyped in terms of the benefits that it provides the U.S. economy.

Sure, it makes America’s imports a little bit cheaper and its asset values a little bit higher, but that comes at the expense of a less competitive export industry.

Instead, for America, the biggest advantage of having the dollar play such an important role internationally isn’t an economic one. It’s the ability to wield a powerful financial weapon that the country can employ through sanctions.

For some people, especially American politicians, this is a priority. They like having a strong dollar because they like the prestige that comes with it and they like being able to flex America’s muscle on the world stage through sanctions or the threat of sanctions.

But when it comes to the average American’s standard of living, the dollar’s international dominance isn’t all that’s it’s cracked up to be.

*others think the decline was inevitable as the economy evolved to focus on higher-value-added products and technologies

**Interestingly, a recent IMF report finds that the U.S. dollar has primarily lost ground not to another major currency, but to smaller currencies like the Australian dollar, the Canadian dollar, and the Swiss franc, as central banks have diversified their foreign exchange reserves