Why The SEC Is At War With The Crypto Industry

If the SEC prevails, the U.S. crypto industry as we know it might cease to exist.

This is the most hated man in the crypto industry today.

His name is Gary Gensler and he’s on a mission to destroy the crypto industry in the United States.

Gensler isn’t just anybody. He’s the Chairman of the Securities and Exchange Commission, the agency that regulates securities markets in the U.S.

Last week, Gensler’s agency filed lawsuits against Binance, the largest crypto trading platform in the world, and Coinbase, the largest crypto trading platform in the U.S., accusing them of violating U.S. securities laws.

If the SEC prevails, the U.S. crypto industry as we know it might cease to exist.

The Howey Test

To understand the battle that’s taking place, first, let’s talk about oranges—yes, the fruit! This will make sense in a minute.

In 1946, the SEC claimed that a man who was selling plots of land with citrus groves on them in Florida was breaking the law.

William John Howey owned hundreds of acres of citrus groves. He kept half of them for himself and sold the other half.

But in addition to the land, Howey offered buyers something else. For an extra fee, his company would cultivate and develop the groves, and it would harvest and market the fruit from the trees as well.

On the surface, this seemed like a simple real estate sale combined with a property management agreement. And that’s the conclusion that the lower courts came to. Howey did nothing wrong, they said.

But when the case eventually made its way up to the Supreme Court, a very different conclusion was reached.

According to the Supreme Court, what Howey was selling wasn’t just land and management services. He was selling stakes in a large citrus fruit enterprise.

The court said that people buying land and services from Howey were in it for the profits. They had no desire to occupy the land or develop it themselves, even though they technically could do those things.

In fact, the plots of land that Howey sold—the average of which was 1.3 acres— wouldn’t be economically feasible to develop independently due to their small size.

Only when they were developed as part of a larger operation, with the right personnel and the right equipment, was it profitable.

Given that, the Supreme Court found that Howey wasn’t selling citrus groves; he was selling investment contracts.

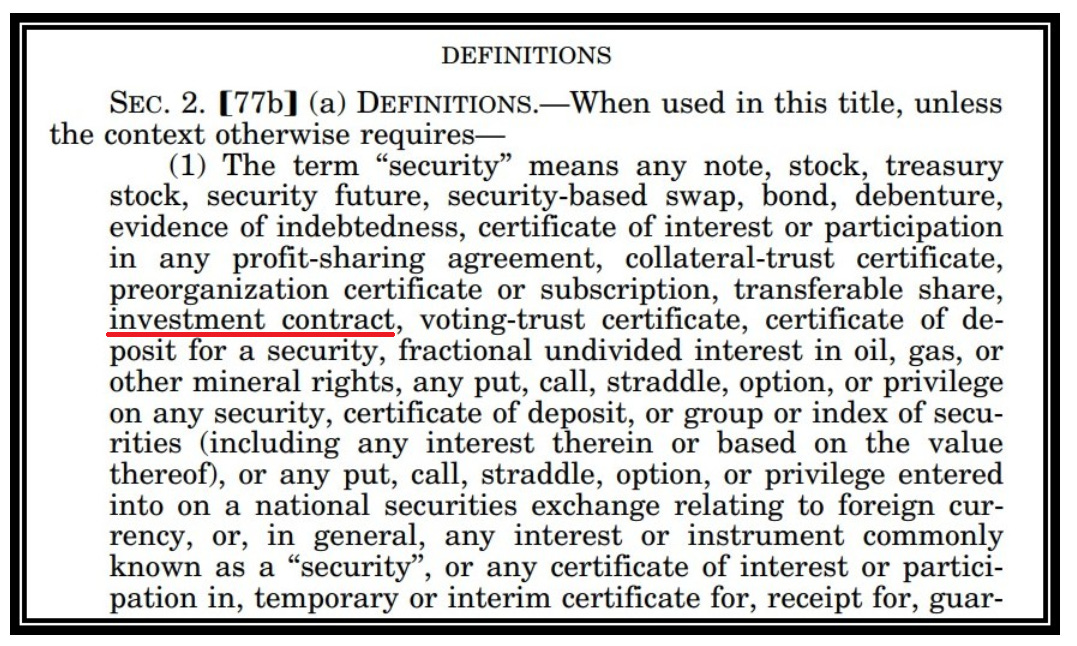

The problem with that is, based on the Securities Act of 1933, investment contracts are a type of security, and securities need to be registered with the Securities and Exchange Commission.

Howey didn’t do that and so he was found in violation of the law.

This is important because this 1946 Supreme Court case has become the basis for determining what is a security and what isn’t a security from a legal standpoint.

Prior to that, people had an idea of what a security was: a financial instrument that represents a contractual relationship between the issuer of the security and the holder of the security.

So, you have securities like stocks, which represent ownership in a company, or bonds, which represent debt.

In the Securities Act of 1933, Congress specifically called out certain types of assets as being securities and the list includes obvious ones like stocks and bonds.

But it also included “investment contracts” in its definition, which up until the Howey Supreme Court decision, was kind of a nebulous term.

That was no longer the case. With its decision, the Supreme Court finally defined the term, and it created a test for determining whether something was an investment contract.

That test, which is now known as the Howey test, is this: if a scheme involves “an investment of money in a common enterprise with profits to come solely from the efforts of others,” it’s an investment contract and by extension, a security.

The orange groves that Howey sold fit that definition: people invested their money together in a business that generated profits thanks to the services provided by Howey’s company.

Crypto Securities

So, what does all this have to do with crypto?

Well, the current SEC Chairman Gary Gensler believes that based on the Howey test, nearly every crypto asset on the market today is a security (with the notable exception of bitcoin, which Gensler and others in the agency consider a commodity).

And because of that, he believes that most crypto issuers—those who sell crypto assets—and crypto exchanges—those who facilitate their trading—are in violation of securities laws.

You see, the SEC’s mandate is threefold. It’s to protect investors; to maintain fair, orderly, and efficient markets; and to facilitate capital formation by ensuring that those with the best ideas can get the financing to make those ideas a reality.

To that end, it makes sure that financial markets are free from manipulation, that company’s financial statements are accurate, and that investors have the key information they need in order to make informed investment decisions.

One of the ways in which the SEC accomplishes its goals is by requiring anyone who sells securities in the United States to register those securities.

Registration entails disclosing information to the public— things like a description of the securities being sold, information about the people behind the securities, the risks associated with purchasing the securities, audited financial statements, etc.

The goal is to provide potential investors with as much information as possible so they can make informed decisions and not get taken advantage of by the issuers of securities.

The Crackdown

So that’s why the SEC exists, but crypto has largely been out of the regulator’s reach. Ever since bitcoin was created in 2009, the crypto industry has been operating outside the purview of the SEC.

That kind of makes sense. Crypto was this brand new thing built on something called a blockchain, and the assets that live on these blockchains aren’t like any other assets we have ever seen.

Because of that, the SEC has had a very hard time keeping up with the industry. Over the past several years, its priority has been rooting out and shutting down obvious crypto scams, which is something that hasn’t been controversial.

No one supports scams.

But the SEC has also made other moves which have received pushback from the crypto industry, such as its lawsuit against Ripple, the creator of the XRP token, in which it argues that Ripple sold XRP in an unregistered securities offering.

The SEC’s argument isn’t that Ripple is necessarily a scam; it’s that it didn’t follow securities laws when it sold XRP.

That lawsuit is ongoing, and a verdict is expected this year.

But regardless of what happens with the XRP lawsuit, that isn’t really a model that the SEC can follow when it comes to the many other crypto assets that it considers to be securities. In the case of XRP, there is very clearly a company that is associated with the token that can be sued for selling tokens to investors without registration.

In other cases, creators of crypto tokens have been much more careful about tiptoeing around securities laws. They’ve sold tokens to non-U.S. investors and to a small number of institutional U.S. investors, like venture capital firms, because those type of sales are exempt from SEC registration requirements.

But after those sales, the tokens eventually make their way onto U.S. crypto trading platforms, where they can be freely purchased by anyone in the U.S.

In the SEC’s eyes, this is an issue because U.S. investors are buying these assets which the SEC considers securities, but they aren’t getting access to the disclosures and protections that they get when they buy traditional financial assets like stocks and bonds.

That’s why the SEC has escalated its crackdown on crypto by suing Coinbase and Binance.

Now instead of going after the issuers of crypto assets, they’re going after the platforms which facilitate the trading of crypto assets.

Coinbase and Binance do a lot of different things, but their primary function is to connect buyers and sellers of crypto assets.

If someone has dollars and they want to purchase ether, they can go to Coinbase and exchange their dollars for ether.

But what the SEC claims in its lawsuit is that almost every token that people can buy on Coinbase is a security, so that makes Coinbase a securities exchange.

And according to the Securities Exchange Act of 1934, securities exchanges must be registered with the SEC.

Because Coinbase hasn’t done that, it’s breaking the law.

Now, there are some other notable details in the SEC’s lawsuit against Coinbase, as well as its lawsuit against Binance—such as claims about how they illegally intertwine exchange and brokerage services (the equivalent of Charles Schwab and the New York Stock Exchange being one entity).

But this idea that the two companies are running unregistered securities exchanges is the most significant charge made against them and it’s an existential threat not just to their U.S. businesses, but to the entire U.S. crypto industry.

Because if crypto exchanges aren’t allowed to operate, it will be extremely difficult for most people to get their hands on crypto assets.

Now, you might be thinking: why don’t these companies just register their exchanges with the SEC and be done with it? How hard could it be?

And that’s kind of what the SEC has been saying. Gensler has said that crypto companies should “come in and register” so that they are in compliance with the law.

But it actually might not be as easy as Gensler and the SEC make it out to be.

As the Committee on Capital Markets Regulation points out, if a crypto exchange registers as a securities exchange, the only thing it can trade are securities that are also registered with the SEC. And since almost no crypto asset today is registered as a security, that exchange wouldn’t be able to offer any assets for trading.

And the fact of the matter is, most crypt assets just aren’t going to be registered as securities, no matter what the SEC says because it’s extremely hard if not impossible for them to do so.

Registered securities have to provide things like public disclosures about “the issuer’s officers and board of directors, the issuer’s business activities, and the issuer’s audited financial statements.”

But in crypto, things like board of directors and financial statements don’t exist.

Likewise, the whole idea of there being an issuer of a crypto asset is also problematic. A crypto asset might have been created by some group of people, but that group might not be involved with the asset anymore.

After all, crypto is about decentralization, where ideally, one person or one group doesn’t have sole control or authority over the ongoing development of the crypto asset and the ecosystem that surrounds it.

Furthermore, registering a token as a security might mean that it couldn’t be used for the purposes it was designed for. Many crypto assets are used for non-investment purposes, such as the purchase of digital goods, as well as enabling the functionality of decentralized software programs.

According to the Committee on Capital Markets Regulation, registering a token as a security “effectively prevents these uses, because the holder of a crypto asset classified as a security could not exchange it for a good or service or conduct a transaction on a blockchain network, unless it did so through a broker-dealer as only broker-dealers can purchase or sell securities.”

In other words, for most crypto assets, registration is practically impossible to do and even if it were possible, it would make those crypto assets effectively useless.

In A Box

The idea of an issuer registering a security and disclosing its business activities, board of directors, and financial statements is applicable to traditional corporations, not most crypto projects, and the SEC has been unwilling to adapt its rules to accommodate the crypto industry.

So crypto exchanges like Coinbase and Binance are in a box. They are being told to register as securities exchanges, but doing so would mean they could only trade securities. But no crypto asset is going to be registered as a security.

Gary Gensler surely knows this and his unwillingness to do anything about it means that a) he either wants to cripple the U.S. crypto industry or b) he truly believes that his hands are tied, but he has no choice but to enforce securities laws as they are written and if that results in the crushing of the crypto industry, so be it.

But regardless of the reason Gensler is doing what he’s doing, the crypto industry has to defend itself aggressively if it wants to survive, and that’s what it intends to do.

Both Coinbase and Binance are going to fight these battles in court, and it will likely take years for them to play out. Ultimately, it could be the courts who decide whether the U.S. crypto industry survives or dies.

But that’s not the only way it could play out. The SEC could change its tune. As long as Gary Gensler is chairman of the agency, that probably won’t happen, but if we see new leadership at the SEC at some point, things could change.

Another possibility is that Congress steps in and passes a law that carves out new rules for the crypto industry that enable it to survive. A draft bill was recently put out by two House committees that would make it so crypto assets could be regulated as commodities rather than securities if the blockchain network associated with the assets are sufficiently decentralized.

Assets could even start out as securities and then later become commodities after their networks become decentralized.

Balancing Innovation & Regulation

I think it makes sense for Congress to step in here. Many crypto assets don’t fit neatly into the traditional securities law framework.

Sure, some crypto assets might have characteristics of securities, but others might be more like commodities, or something else entirely.

Ether, for example, has characteristics of a currency, a commodity and a staking asset.

So I don’t think it would be a good idea for the U.S. to shut down the crypto industry and lose all the potential that comes with it.

It would be bad for innovation and the competitiveness of the United States. After all, these assets and these technologies won’t go away. They’ll just be used in other countries that take a more welcoming approach to the crypto industry.

But I get it—a lot of people don’t like crypto. They think it’s a scam at worst and useless at best.

I agree that scams should absolutely be rooted out. But the market should decide whether something is useful or not.

It's about finding the right balance between innovation and regulation.